Unlock Premium Content – For just $0.39/day ($12/month) or $0.27/day ($100/year)!

🔗 Portfolio Corner - 🗓️ Monthly Updates (Last Update: 25-Jun-2026)

I‘ve been spending quite a bit of time lately digging into European quality SMBs, and Norbit ASA keeps standing out as one of those businesses that just works.

What started as a small engineering shop in Trondheim in 1995 has evolved into a specialized technology company with emerging, and credible, competitive advantages across three distinct segments (specially one of them). Considering how much attention small-cap serial acquirers get on FinTwit and among retail investors, it’s still surprising how under the radar this one remains.

That said, assessing the durability of the business isn’t entirely straightforward right now. Norbit is benefiting from multiple tailwinds simultaneously, and the key question (the one that actually matters for whether you should own this or not) is whether those tailwinds are temporary or structural.

I’ll come back to that. But whatever the answer turns out to be, Norbit’s success so far has come from its ability to carve out defensible niche positions where being small is actually an advantage. That’s been the core playbook to date. As the company continues to scale, even management has acknowledged in its latest earnings report that the strategy may need to evolve, and I think that acknowledgement is worth paying attention to.

The company operates across three segments: Oceans, Connectivity, and Product Innovation & Realization (PIR). All three share a common technological backbone: embedded electronics, sensing, and signal processing. These were assembled with the idea of deploying the same core capabilities across different end markets, each experiencing its own macro tailwinds at roughly the same time.

Topics I’ll Cover

🔹 The People Behind the Machine

🔹 Three Segments to Win Them All + The Hidden Optionality

🔹 Financials: Tech Margins on Industrial Products

🔹 FY2025 & Q1 2026 earnings digest

🔹 Cash-on-Cash Return Model

🔹 My DCF Model & Analysis

🔹 The Long-Term Question: Sustainability at Scale & Whether I am Buying or Not (🔐 available for subsribers)

Let’s dig in.

📚 Articles

🔎 Deep Dive Briefs

⛅ Cloudflare | 👷♂️ Parsons | 𓇲 MPS | 🥼 Medpace #1, Medpace #2 | 🔌 Arista | 🛒☁️ Amazon | 🤖 ASML | 🦎 Topicus | 💡 Lumine | ✈ HEICO | 🧙♂️ CSU Part #1, Part #2, Part #3 | 🤖 Intuitive | 🛒 💳 MELI Part #1, Part #2, Part #3 | 💻 Cadence | 🌊 Norbit

💸 General Investing

💎 Hidden Gems Series

✨ Annual Specials – Annual Letters, Investing Philosophy, Industry Write-ups & Top Picks of the Year

📚 Resources for Investors

📢 Latest Stock News → Earnings Digests & other related news

💬 Join My Chat → [🔗 Learn more]

🔐 Paid Subscriber Exclusives

💼 Portfolio Corner – Holdings, valuation models, trades, performance & more!

🤫 Exclusive Sections – From select articles, Deep Dive Briefs & Hidden Gems

👀 Recent Releases!

💸 Software Darwinism, Software Darwinism 2.0 & Software Darwinism 3.0 → We talk AI, SaaS, VMS and Where the CSU family stands

💎 Hidden Gems: Sixth Edition → A Primer on TerraVest Industries

👀 Coming Soon

🔎 Two-parts Deep Dive Brief: Palantir

💎 Hidden Gems: Special Edition IV —> A Robotics play in the defense space.

💎 Hidden Gems: Seventh Edition —> 2 Nordics Niches, early stage.

New Article Format Coming: Short analysis briefs on the watchlist stocks I currently find most interesting (or am digging into more deeply):

where I see the opportunity,

what I like,

and what keeps me from pulling the trigger.

(Will be partially open to read, the rest will be kept available for paid subsribers).

The People Behind the Machine

Before we get into the numbers, we need to understand who is running this business. CEO Per Jørgen Weisethaunet joined as one of the first employees in 1995 and has been at the helm since 2001. That’s 24 years leading the same company. Founder Steffen Kirknes still controls 15.5% of shares, and Per Jørgen owns roughly 11%.

Total insider ownership sits above 25%.

As you may already know from the companies I like to cover, this matters. A lot. When management has this much skin in the game, capital allocation decisions take on an entirely different character. These are owner-operators thinking in years, not in quarters.

Culturally, the company revolves around a single guiding principle: “Explore More.”

I’ll admit that this kind of thing can easily read as generic corporate speak. But Norbit has backed it up with pristine execution since its 2019 IPO:

+900% total returns over five years,

revenue compounding at a 32% five-year CAGR,

EPS compounding at 67%,

and a market cap that has grown from roughly €100 million at IPO to over €1 billion as of 2026.

Numbers like that don’t emerge from a culture that’s merely decorative. As Per Jørgen put it:

“Talent and culture have always been at the heart of our priorities. Ensuring that we continue to attract the right people, offer them the right seat, and create an environment where they can grow… is essential for the journey ahead.”

In businesses like Norbit’s, people (mostly engineers) are the moat as much as the products. I don’t think this point gets enough attention in the market, but I do.

Three Segments to Win Them All

Playing Small & Smart: The Oceans Segment

The 🔗 Oceans segment (35% of FY2025 revenue, now below 30% post-Q1 2026 results) develops ultra-compact wideband multibeam sonars used to map the seabed, inspect underwater infrastructure, and support offshore energy projects.

This is not a market without competition. Kongsberg Discovery and Teledyne Marine dominate large-scale sonar suites and system integration, and they are not going away. But here’s where it gets interesting: Norbit wins by not competing with these players directly. Instead, they focus on compact, integrated sonar solutions for commercial and security markets where the legacy giants are simply too large and too slow to be relevant.

Think of it this way. Just as computing evolved from room-sized mainframes to pocket-sized devices without losing power, acoustic underwater systems have undergone a similar transformation. Norbit specializes in making sonars that are smaller, more integrated, and easier to deploy. Their market position is reinforced by a sophisticated customer/partner ecosystem. Rental companies like Ashtead Technology and Norwegian Offshore Rental act as distribution arteries, lowering the barrier to trial.

Acquisitions of Ping DSP (side-scan sonars) and Innomar (sub-bottom profilers) have outperformed expectations by plugging smaller companies into Norbit’s global sales network.

A Hidden Catalyst: Unmanned Vehicles & Forward-Looking Sonars

While multibeam echo sounders are the bread and butter, the most compelling optionality lies in Forward-Looking Sonars (FLS) and their integration into unmanned underwater and surface vehicles (AUVs).

The U.S. Navy recently awarded prototype agreements to build Large Displacement Unmanned Underwater Vehicles, and Norbit is on the list of technology providers, supplying FLS to both the Anduril Dive-LD and Oceaneering Freedom. Turkey’s STM has revealed the NETA 300 autonomous underwater vehicle utilizing Norbit’s Compact FLS.

Here’s why this matters, and it’s something I think the market might be underpricing it at the moment. Historically, the Oceans segment had very low customer concentration. Survey companies typically operate three to four vessels, meaning significant effort was required to sell each individual unit.

Unmanned vehicle adoption changes this dynamic completely. When Norbit secures a design win for an autonomous platform program, the sales costs are largely fixed while volumes scale. The co-development and integration costs are already in the cost base. That leaves room for very high incremental margins as military and commercial programs transition from prototype to serial production. This is a very different revenue profile than selling one system to 50 different survey customers.

We’re still in the early innings. Hard to know how large the opportunity ultimately becomes for Norbit’s ocean segment, but the optionality here is compelling to say the least.

Connectivity: The Regulated Rails

The 🔗 Connectivity segment (25% of total revenue) occupies a precise niche between two unattractive positions. Above them sit chip suppliers like Quectel and u-blox, who lack the integration and regulatory competence to move downstream. Below them are heavy ITS players like Kapsch and Q-Free, whose economics are burdened by large-scale public contracts.

Norbit builds the high-margin (25%-30%) certified On-Board Units that power Europe’s tolling networks. Smarter, lighter, and far more profitable than what the giants would bother making.

The regulatory environment continues to work in their favor. In Q4 2025, the segment received a new order worth NOK 160 million for deliveries to Toll4Europe, one of the leading European Electronic Toll Service providers.

Despite the very strong numbers and the company’s seemingly advantageous positioning today, I’m not overly excited about this segment. Main reason: I don’t yet see a truly durable competitive advantage despite the regulatory tailwinds like the one stemming from the Oceans segment, i.e. engineering know-how, structural tailwinds, embedded expertise, etc.

Time will tell.

PIR: The Manufacturing Muscle

The 🔗 Product Innovation & Realization (PIR) segment (now closer to 40-45% of total revenue over the last 4 quarters) combines in-house R&D, design, and high-end electronics manufacturing.

The market for precision contract electronics is crowded. Regional EMS giants and defense primes populate it. But the competition here is not about who can build cheaper. It’s about who can build smarter, with better compliance, confidentiality, and agility. As Europe scrambles to secure supply chains, rebuild strategic manufacturing capacity and develop defence muscle, PIR has emerged as one of Norway’s most sophisticated design-to-production platforms. In Q4 2025, PIR revenues grew 174% YoY. Growth in Q1 2026 still remained above the 100% mark, driven by strong defense and security demand, while the segment continues to receive large orders.

PIR also acts as a stabilizer, keeping development and production capabilities fully utilized even when demand in the product segments fluctuates. There’s a secondary benefit that doesn’t get discussed enough: the same precision manufacturing that serves defense customers can be deployed across Norbit’s other segments, reinforcing the entire platform.

I do like this segment, despite the lower margins versus Oceans and Connectivity (~15–20%). That said, as I’ll discuss later on, it is fundamentally changing the nature of Norbit’s historical business.

Financials: Tech Margins on Industrial Products

Norbit’s profitability profile reflects its hybrid identity, part industrial manufacturer, part technology company. Gross profit margins typically hover between 55–60%, a clear signal that Norbit’s products carry real pricing power. Customers pay up because failures would be far more expensive than the system itself. Operating margins have expanded from historical averages around 12% to a range of 17–25% recently, demonstrating its operating leverage as the company scales.

The cash flow inflection has also been outstanding. Between 2022 and 2024, as supply chains normalized and excess safety stock unwound, free cash flow transformed from roughly NOK –30 million to NOK +286 million in 3 years. This is a business that not only grows but does so on its own cash flows. Just what you want to see.

ROIC has more than doubled since 2020 and is trending north 20%, well above any conservative estimate of cost of capital. Same goes for ROCE trending now above the 30% mark.

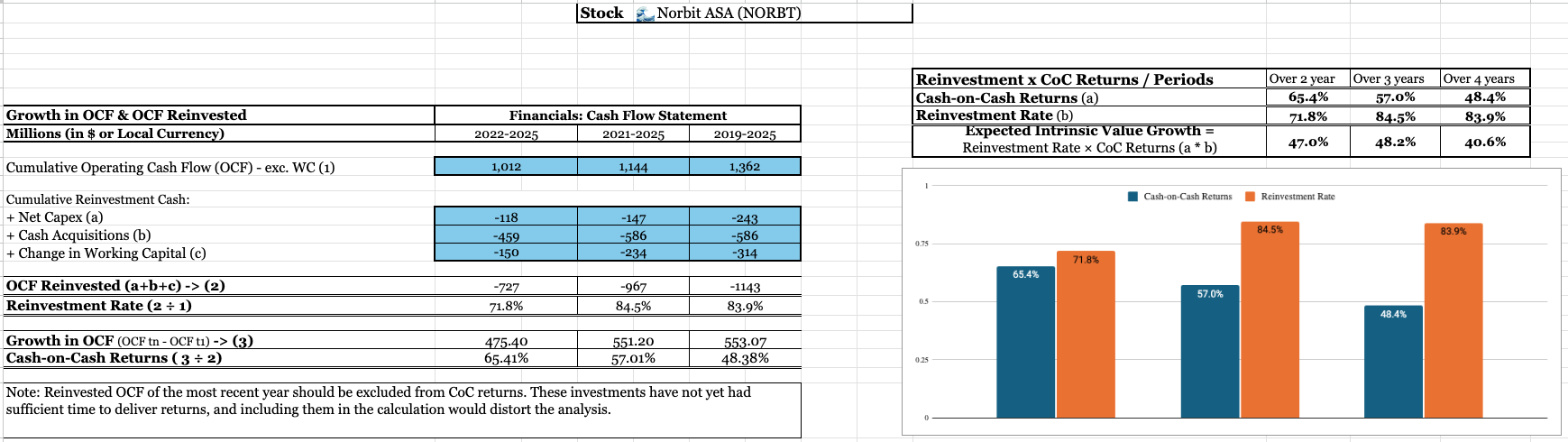

Also, I modelled out Norbit’s 🔗 Cash-on-Cash Returns recently, here are the results:

Impressive numbers since going public in 2018. High reinvestment rates coupled with strong cash returns on invested capital.

The FY25 Blowout

If there was any doubt about Norbit’s operating leverage due to the competitive nature of the segments it operates in, the FY2025 results erased it:

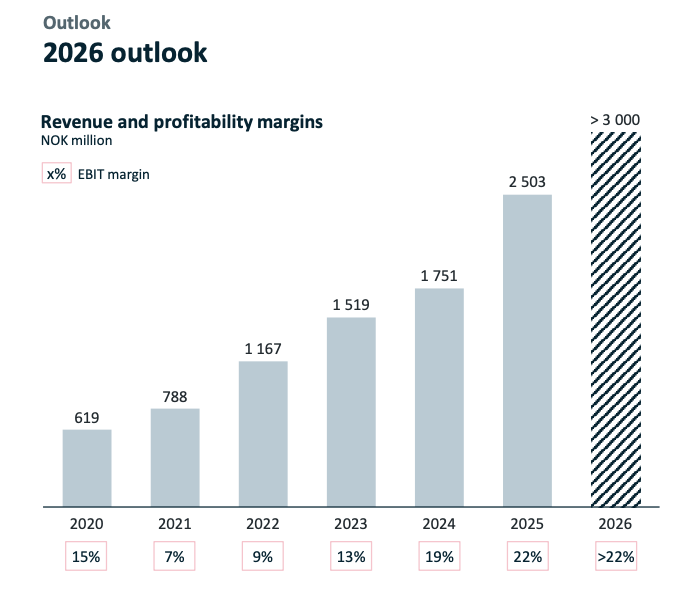

Record revenues of NOK 2,502.5 million, up 43% from 2024

EBIT of NOK 555.4 million with a 22% margin

Pre-tax ROCE averaging 34% for the year, hitting 41% in Q4

Diluted EPS growing 61% to NOK 6.32, with a proposed dividend of NOK 5.00 per share, 79% of earnings. Wait… what ?! 👀 Don’t get scared by it, his is fairly typical Nordic-style capital allocation 😄. Personally, I do not like it.

Management pulled forward its own guidance. In February 2024, Norbit set an ambition to deliver more than NOK 2.75 billion in revenues by 2027. Based on current performance, they are now targeting more than NOK 3.0 billion for 2026, one year ahead of schedule.

Q1 2026 Numbers: Thesis Breaking ?

Norbit reported Q1 2026 a few weeks ago. Oceans revenue fell 12% YoY due to lower-than-expected shipments of its high-value Winghead sonars, gross margin compressed from 62% to 53%, and the stock dropped from ~230 NOK to 175 NOK afterwards.

The market’s framing seems straightforward: the “smart niche compounder” thesis is cracking. I understand the concern, but I think it’s far too early to draw that conclusion.

Management explained that the YoY decline in Winghead sales was largely driven by unusually strong rental company demand in Q1 2025, creating difficult comps. This is not a recurring revenue business (there is inherent lumpiness in customer orders) and Q1 last year was exceptionally strong.

More importantly, the long-term thesis here was never about short-term nosie around sonar shipments. The question is whether Norbit’s compact curved-array multibeam sonars become a critical enabling component for autonomous underwater vehicles (AUVs). And on that front, the company remains well positioned.

Norbit is one of the few suppliers globally with this specific product positioning. If Copperhead-class AUV platforms (like the ones built by Anduril) scale toward expected procurement volumes over time, the addressable opportunity for this product line alone could become meaningful. None of that optionality appears reflected in current numbers yet.

To me, the Q1 weakness looks more like timing noise than structural deterioration. The actual structural opportunity in Oceans still lies ahead.

The more difficult question is whether Norbit is gradually changing the nature of its business model. And if so, whether that shift is positive or negative.

PIR grew 110% YoY on the back of European defense contract manufacturing. Connectivity grew 45% YoY. Both making up more than 70% of Norbit’s business. Meanwhile, Oceans (historically the company’s highest-margin and strongest moat segment) now represents roughly 30% of revenue, down from 50%+ a few years ago.

So if you originally bought Norbit expecting a pure-play niche sonar/IP business, what you increasingly own today looks closer to a defense and electronics components contractor with a premium sonar segment attached to it.

The gross margin compression is the clearest evidence of this mix shift.

Personally, I don’t necessarily view that as a problem, but I do think it changes the thesis somewhat.

Norbit now sits at the intersection of several powerful secular tailwinds:

European defense spending is entering a multi-year capex cycle, benefiting execution-focused manufacturers like PIR

Underwater autonomy appears to be transitioning from R&D budgets toward procurement budgets, where incumbents with proven products tend to win design slots. Here is where Norbit’s ocean optionality lies.

That gives Norbit two relatively independent growth vectors : one that’s already real and seen in the numbers, the other one that’s just a prospect.

The key debate becomes whether the Oceans optionality ultimately scales enough to offset the lower-margin mix coming from PIR. Because while both segments may drive growth, the quality of earnings is clearly different.

Importantly, I’d argue the market has already started pricing this uncertainty in.

Since mid-2025, the stock has largely consolidated its multi-year run and now trades around 175 NOK, roughly ~20x 2027 earnings estimates for a business that is expected to grow revenue over the next two years at a ~20% clip with a more-than-plausible path toward NOK 3B in annual sales this year.

At that valuation, you’re still paying for a growth compounder, but no longer at the kind of euphoric premium the stock commanded last year. That discount itself may become the opportunity.

As some people on X argued recently, a different business mix probably deserves a different multiple over time. Contract manufacturing businesses typically trade closer to 10–15x earnings, while IP-led niche technology platforms can command 25–30x. A blended Norbit likely lands somewhere in between.

At ~20x forward earnings, the valuation feels fair for today’s mix, though I’d expect some multiple compression over time if PIR continues to outgrow the higher-margin Oceans segment.

My DCF Model: What Are We Actually Paying For?

Management already expects some margin compression this year due to the changing segment mix. For the sake of this analysis, though, I’ll take a more optimistic stance and assume the AUV thesis gradually plays out over the next few years.

Under that scenario, Oceans would slowly regain prominence and trend back toward ~40% of total revenue, with Connectivity stabilizing around 25% and PIR around 35%. That mix would likely push consolidated margins back toward the 23–25% range over time.

Using embedded assumptions of ~18% top-line growth over the next 5 years, followed by ~15% growth through year 10, this translates into roughly:

• NOK 1B in NOPAT by 2030

• NOK 2B in NOPAT by 2035

Assuming the company is still capable of sustaining double-digit growth by then, a ~20x earnings multiple could remain reasonable, especially when combined with the long-duration optionality tied to underwater autonomy and AUV adoption.

Put differently, the setup can still work from current levels if you’re patient enough and willing to underwrite the Oceans optionality.

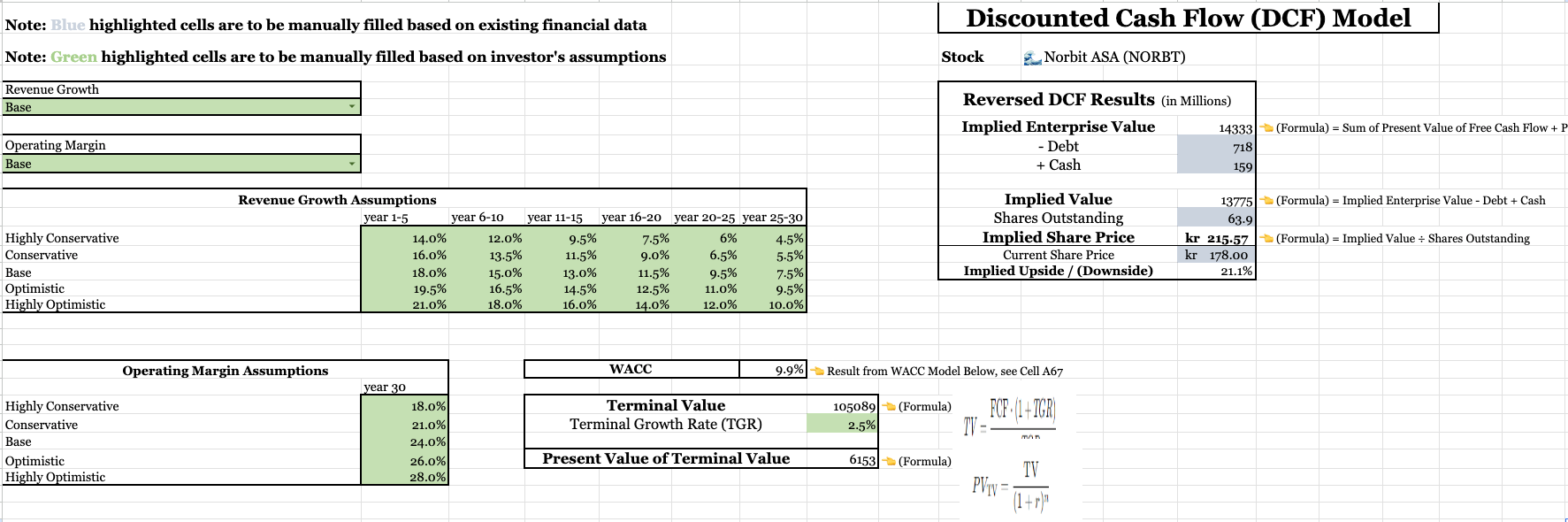

If we translate these assumptions into a more balanced base-case framework and run them through a 30-year DCF model, we get the following results:

This +21% implied upside was based on a ~178 NOK share price for Norbit at the time of analysis, suggesting attractive return potential from current levels.

That said, reality could easily prove less optimistic.

Growth may slow. PIR could become the dominant segment over time. The AUV optionality may take far longer to materialize or fail to materialize altogether. There are still plenty of “ifs” embedded in this thesis.

But if Norbit’s management continues executing with the same discipline and operational quality they’ve demonstrated so far, I suspect investors will continue rewarding the business and get rewarded by the stock price.

The key difference is that future returns will probably look different from the extraordinary rerating-driven gains of the past five years. From here, compounding is likely to depend far more on execution, segment mix evolution, and whether the Oceans optionality ultimately scales into something material.

🔐 DCF & Reversed DCF + Growth & Capital Efficiency Models (ROIC, ROCE and Cash-on-Cash Returns models) — Available for Paid Subscribers

The full NORBT valuation suite, including the DCF model ready for download along with 30+ names and Capital Efficiency models (ROIC, ROIIC, ROCE, CoC Returns), and Growth Models (Reinvestment Rate × ROIIC to estimate intrinsic value growth) for over 40 names tracked on Expanse Stocks, are available for download here: 🔗 Portfolio Corner

The Long-Term Question: Sustainability at Scale & Whether I am Buying or Not

The question isn’t whether Norbit is a well-managed business, it clearly is. The real question is whether it can sustain exceptional returns as it inevitably scales into markets where larger competitors start paying attention.

My opinion: