Deep Dive Brief: HEICO

Compounding in the Sky

Unlock Premium Content – For just $0.39/day ($12/month) or $0.27/day ($100/year)!

🔗 Full Portfolio Content - 🗓️ Biweekly Updates (Last Update: 28-Jun-2025)

Expanse Stocks x Finchat (now Fiscal AI) Partnership!

🎁 Get 20% off + 2 months free on any Finchat plan! →🔗 Claim Discount

Welcome back Explorer!

In this tenth edition of my Deep Dive Briefs series, I’m continuing my research journey on serial acquirers—this time exploring:

Last Month, I published two Deep Dive Briefs on Topicus (the first of CSU’s spin-offs), and Lumine Group (the second CSU spin-off). If you haven’t had a chance to read them yet, here are the links:

🔗 Hidden Gem Deep Dive Brief: Lumine

🔗 Hidden Gem Deep Dive Brief: Topicus

In this edition, we’ll dive into one of those rare companies with a durable, strong reinforcing moat, a long growth runaway, with some of the best owner-operators at the helm.

Topics I’ll Cover

🔹 Company Overview

🔹 History, Leadership & Culture

🔹 Core Offerings & Business Model

🔹 Economic Moat

🔹 Growth Drivers

🔹 Capital Allocation Strategy

🔹 Risks & Challenges

🔹 Valuation Model - Quick mental framework and DCF model to estimate intrinsic value and shareholders returns

🔹 Final Thoughts – My stance on HEICO as a long-term investment

This deep dive brief is open to everyone. I hope you enjoy it, let’s dive in!

📰 What’s New at Expanse Stocks?

📊 Quarterly Update - Portfolio Composition (by Industry and Geography) + Valuation Metrics → 🔗 Behind-The-Scenes [Free access]

📚 Articles

🔎 Deep Dive Briefs

⛅ Cloudflare | 👷♂️ Parsons | 𓇲 MPS | 🥼 Medpace | 🔌 Arista | 🛒 Amazon | 🤖 ASML | 🦎 Topicus | 💡 Lumine | ✈ HEICO

💸 General Investing

💎 Hidden Gems Series

✨ Annual Specials – Annual Letters, Investing Philosophy & Top Picks of the Year

📚 Resources for Investors

📢 Latest Stock News

💬 Join My Chat → [📎 Learn more]

👀 Coming Soon

💆♂️ A Reflection on my Investing Mistakes

💸 The Power of Optionality

➕ Unlock Premium Content – For just $0.39/day ($12/month) or $0.27/day ($100/year)!

🔗 Full Portfolio Content - 🗓️ Biweekly Updates (Last Update: 28-June-2025)

📈 Biweekly Report – Portfolio updates, recent moves & watchlist additions

💼 Full Portfolio Access – Holdings, valuation metrics & performance tracking

📊 Valuation Tools – DCF, reverse DCF, capital efficiency & growth models

🎧 Podcast Picks – Biweekly handpicked episodes on business & investing

🔎 Stock Picking Framework – My methodology & investing philosophy

🎯 Swing Trading – Short-term strategy & latest swing trades

💬 Private Community Chat - 📎 Learn more

🔐 Full access to all my articles

Company Overview: Niche Conglomerate

Heico Corporation is a niche juggernaut specializing in the aerospace and defense components for the commercial aerospace aftermarket.

Founded in 1957 and transformed by the Mendelson family in 1990, Heico’s model has all the looks of a mini-Berkshire:

Lean corporate HQ and autonomous subsidiaries

Disciplined M&A

An obsession with free cash flow

The company operates through two core business segments:

Flight Support Group (FSG): ~70% of revenue — develops and sells FAA-approved Parts Manufacturer Approval (PMA) components, primarily for the aerospace aftermarket.

Electronic Technologies Group (ETG): ~30% of revenue — manufactures niche high-reliability electronic components used in defense, space, and medical devices.

The company's core playbook?

Finding complex, low-volume, non-commoditized components that are mission-critical with long lifespans, reverse-engineer them at lower cost, pass 🔗 FAA certification, and deliver them at a 30–50% discount to Original Equipment Manufacturers (OEMs) — all without compromising safety and with a value proposition airlines and governments increasingly appreciate.

Today, HEICO stands as a global operator with a highly decentralized structure, the undisputed leader in the PMA space, and a portfolio of over 100 subsidiaries.

Its dual-class share structure ($HEI, $HEI.A) has allowed the Mendelson family to maintain long-term strategic control with greater voting rights and without short-term shareholder pressure, while still providing public investors access to one of the most consistent mid-cap compounders in the industrial sector.

🧐 Fun Fact: The HEI vs. HEI.A Price Gap

As of June 2025, there’s a notable 21.6% discount between HEICO’s two share classes:

HEICO (HEI): Full voting rights (1 vote per share)

HEICO A (HEI.A): Limited voting rights (1/10th vote per share)

The official reason? Voting rights. HEI shares offer more control over the company, which theoretically justifies a premium.

But here’s the thing:

A 21.6% premium for just extra voting rights—when the Mendelson family effectively controls the company anyway—seems excessive.

The economic rights (dividends, ownership) are the same for both classes. So, unless you’re an activist investor or looking for control (which is essentially impossible here), it’s hard to argue that HEI shares are worth 20%+ more.

Bottom line:

For long-term investors focused on economic return—not control—HEI.A shares offer better value. And historically, this price gap has tended to revert somewhat over time, occasionally offering an arbitrage-lite opportunity.

History & Evolution: From Struggling Lab Equipment to Aerospace Conglomerate

Heico was founded in 1957 as Heinicke Instruments, originally focused on laboratory equipment. Its transformation began in 1974 with the acquisition of Jet Avion, a manufacturer specializing in jet engine components, marking Heico’s first step into the aerospace sector.

A key moment arrived in the 1980s, following a commercial airline accident that revealed design flaws in jet engine combustors—one of the engine’s most critical and sensitive parts. With OEMs unable to meet the sudden replacement demand, the FAA and major airlines turned, for the first time, to a PMA supplier: Heico. The company reverse-engineered the combustor components, and their quality passed every test. The trust earned during this period became a cornerstone of Heico’s reputation.

But the company’s true inflection point came in 1990, when the Mendelson family—led by Larry Mendelson and his sons Eric and Victor—acquired a stake in the struggling lab equipment firm. Through a leveraged buyout, they gained control, quickly divested the legacy business, and began transforming Heico into the aerospace powerhouse it is today.

Recognizing a regulatory gap, the Mendelson family saw a unique opportunity in the aftermarket for aircraft components—an industry then dominated by OEMs known for high prices and slow delivery times. Their insight was simple: if Heico could successfully reverse-engineer and certify a complex combustor, why not expand that capability across a broader range of components?

Over the next three decades, Heico built a portfolio of FAA-approved PMA parts and executed more than 100 acquisitions—primarily founder-led, cash-generative businesses in niche markets. This strategy has compounded into over 20,000 FAA-approved components, with 500+ new approvals annually, and an estimated 50% share of the global PMA market.

From its first $2m bolt-on deal to its $2B biggest acquisition of former competitor Wencor in 2023, Heico’s M&A strategy has remained intact: acquire durable businesses at reasonable multiples, retain their culture and leadership, and empower them to grow under Heico’s decentralized umbrella.

What began in the 1980s and ’90s as a niche aftermarket parts supplier has evolved into a diversified aerospace and defense components ecosystem, built on regulatory trust, an impeccable safety record, and world-class capital allocation under the stewardship of the Mendelson family.

Leadership & Culture: The Mendelson Dynasty

Heico is a family affair and proud of it.

Larry Mendelson (Chairman/CEO): Led since 1990. Deeply hands-on. Corporate culture reflects his low-ego, long-term style.

Victor Mendelson (ETG Co-President): Oversees high-tech defense units. Long tenure and technical savvy.

Eric Mendelson (FSG Co-President): Architect of Heico’s PMA dominance.

Together, they’ve grown Heico from a $25M market cap in 1990 to a $37B aerospace powerhouse, or a whooping +147 900% total return.

Culturally, Heico is a rare breed, representing capitalism at its best:

Long-term focus: Key to Heico’s brand is customer trust, not pricing power. The Mendelsons favor margin restraint in exchange for loyalty.

Decentralization with discipline: Roughly 80% of acquired subsidiaries are still led by their original founders. Heico’s headquarters remains intentionally lean, centralizing capital allocation but leaving execution to local operators—minimizing bureaucracy and empowering autonomy.

Reputation for fairness: Price increases are modest (low-single digits), while Heico maintains industry-best turn times and inventory availability, even for lower-volume parts.

Acquirer of choice: Many founders come directly to Heico when they consider selling—drawn not just by valuation, but by the company’s track record of respecting legacy and people

And above all, their values are simple and powerful:

Underpromise, overdeliver.

Leave money on the table if it earns trust.

Bet on people, not spreadsheets.

As Larry Mendelson puts it:

“We could charge more… but we don’t. We leave money on the table in the short term to build something permanent.”

Core Offerings & Business Model

Heico operates via two segments:

Flight Support Group (FSG) – 68% of revenue

Designs, manufactures, and sells PMA parts for the aftermarket of aircraft engines and airframes

Offers MRO (maintenance, repair, overhaul) services

Distributes both PMA and OEM parts for airlines and lessors

Acquired Wencor (2023), the #2 PMA player, doubling the scale of the PMA business

Business Dynamics:

OEMs usually sell original components/parts at a loss to secure future maintenance revenue.

Heico reverse-engineers those parts and sells at a 30–50% discount, with FAA approval. This aircraft aftermarket business is a space known for its relatively high margins and long equipment lives. On top of that, Heico offers MRO services providing recurring revenue streams.

PMA parts support aircraft aged 10–25 years, a sweet spot where OEM pricing is punitive, and reliability trumps brand loyalty.

Today, Heico has 19 of the top 20 airlines globally as customers.

Electronic Technologies Group (ETG) – 32% of revenue

Supplies custom-engineered niche electronic and electro-optical components for high-reliability applications. Products include laser range finders, sensors, power systems, RF modules often integrated into complex systems (satellites, missiles, targeting equipment).

Customers span defense primes, commercial space, and medical device makers. Some clients include NASA, Raytheon, Lockheed Martin, SpaceX, and Medtronic.

Acquisition-driven segment with the majority of ETG's businesses run autonomously by the original owners.

Competitive Edge

ETG provides mission-critical, low-cost components with small volume but high strategic importance.

PMA approval process can take years. Therefore, competitors are unlikely to match Heico’s throughput.

FAA has granted Heico “Organizational Design Authorization” (ODA), allowing internal self-certification of parts — a rare privilege.

Airlines and defense customers prize reliability: Heico has never had a flight safety bulletin on any part sold.

Common Threads Across Both Segments

Unmatched scale

Trust with the FAA

Deep customer trust

Zero-failure tolerance

On-time part availability

High regulatory/technical barrier to entry

A very fragmented supplier base ripe for opportunistic ‘roll-up’ acquisitions

Economic Moat

As already hinted at in the previous section, Heico’s competitive advantage is built around:

Intangible Assets: Deep know-how in reverse engineering and FAA regulatory navigation.

Regulatory Approval Process (FAA PMA): Takes years to develop, test, and certify a part. Most players can’t afford the investment or the wait.

Switching Costs: Airlines and defense primes are deeply risk averse, they don't swap critical parts providers lightly. Once a PMA part is qualified, they rarely revisit the supplier list.

Distribution Reach: Direct-to-airline relationships and in-house logistics

R&D, Safety and Trust: It takes years of perfect performance to earn the FAA's and customers' trust — something no competitor has yet matched at scale.

Organizational Designation Authorization (ODA): A rare FAA privilege allowing Heico to self-certify parts which allows them to significantly accelerate time-to-market.

Safety Record: Over 85 million parts shipped with zero safety bulletins. This is nearly impossible to replicate.

The PMA portfolio is also highly diversified — no single part or customer dominates, which helps insulate earnings.

Growth Drivers

Heico’s growth engine is built on a mix of organic expansion, regulatory arbitrage, and M&A

PMA TAM Expansion: PMA parts are still only 2–4% of the $65B+ MRO market, with room to 3–4x. Lufthansa (their very first customer) shows >10% penetration is feasible.

Fleet Aging: Airlines are holding onto older aircraft longer post-COVID, driving more maintenance cycles. As fleet retirements are delayed, PMA parts become more valuable.

Leasing Evolution: Lessors (who own 50% of the fleet) are warming to PMAs. This is a major unlock for market expansion.

OEM Pressure: Airlines are pushing back on anti-PMA warranties. Regulatory bodies (like IATA) now limit OEM anti-competitive behavior, clearing space for Heico.

M&A Engine: Completed 100+ acquisitions — targeting 3–7 deals per year. Acquisitions typically done at 1.5–3x sales, with 15%+ IRRs + Founders now approach Heico directly due to its reputation.

Cross-Selling with Wencor: The 2023 $2B acquisition of Wencor brought 6,000 more PMA parts, broader customer base, a parallel distribution channel, and a potential $100M synergy in supply chain, repair, and sales.

Defense Spending: ETG is tied to high-priority defense systems. Radar, satellites, missiles — these are strategic, funded programs.

Capital Allocation: A Masterclass

The Mendelson family has been providing a generational masterclass in long-term capital allocation:

M&A Returns: Over 100 acquisitions since 1990. Nearly all profitable. IRRs in the mid-teens.

FCF Reinvention: >100% of FCF reinvested into acquisitions over the last 15 years. This includes tuck-ins and platform buys.

Improving ROICs on acquisitions: Mid-teens and growing, especially in defense (ETG), with returns on tangible capital (exc. Goodwill + Intangibles) estimated around 30+% (maybe higher).

Low Leverage: Debt/EBITDA stays between 0.25x and 2x — even through COVID and after large deals like Wencor.

No Buybacks, Symbolic Dividend: Capital goes to growth, not shareholder appeasement. Dividends (sub-0.5% yield) are symbolic.

Price Discipline: They walk away from deals that don’t meet return hurdles. They don't overpay. They prefer founder-led businesses and they’re in it for the long haul.

For the Mendelson family, acquisitions are culturally embedded in the business. Heico actively seeks out founders who want to stay on and continue building. That’s why more than 80% of acquired leaders still run their businesses today.

If you’ve been following Expanse Stocks, you know how highly I regard Constellation Software’s founder, Mark Leonard, as a capital allocator. But truth be told, the Mendelson are operating at a similarly elite level, just in a different arena.

Risks & Challenges

PMA Adoption: Still sub-5% penetration — maintenance teams are slow to change vendors, even when savings are obvious.

OEM Pushback: While regulatory bodies are supporting PMA, large OEMs are still aggressive in contract structuring.

Defense Budgets: ETG’s future depends on long-cycle U.S. government procurement. Prioritization changes could hit certain product lines.

Succession Planning (underway): Larry is 86 years-old — though Victor and Eric are well-prepared, transitions always carry risk.

M&A Dependence: Heico’s growth partially depends on acquisition cadence and integration. Execution risk grows with deal volume and complexity — especially post-Wencor.

Financials & Valuation - Includes Mental Framework to Estimate Returns and DCF Models

HEICO has shown impressive financial metrics for years:

🔹 Consistent Top line Growth

With a $38B Market cap, Heico has achieved revenues (TTM) of ~$4.1B with a 5-Year Avg. Revenue Growth of ~16%.

Excluding the COVID-19 anomaly, HEICO has steadily grown revenues in the mid- to high-teens for many years. This growth is driven by a balanced mix of:

Organic Growth: High-single digits

Inorganic Growth (M&A): Mid-single digits

Management has consistently reinvested >100% of free cash flow, and with a still-large unpenetrated TAM in both PMA (Parts Manufacturer Approval) and ETG (Electronics Technology Group) segments, there’s a long runway for continued compounding—potentially decades.

🔹 Healthy, Predictable Margins: EBITDA Margin: ~26–28% | Free Cash Flow Margin: ~18–20%

Margins have remained consistent without relying on aggressive pricing tactics. In contrast to TransDigm, HEICO maintains a strong reputation for fair pricing and high product quality, reinforcing long-term customer trust.

🔹 High Returns on Capital: ROIC (incl. Goodwill): ~12–15% | Returns on Capital (ex-Goodwill prior to Wencor acquisition): ~25-30%

Management enforces a strict capital allocation discipline, similar to Constellation Software, targeting IRRs in the mid-teens or higher on acquisitions—an approach that has created long-term shareholder value and high returns on investment without overreaching.

🔹 Conservative Balance Sheet: Net Debt/EBITDA: ~1.8x (post-Wencor deal) | Target: Normalized <1.0x

HEICO’s use of leverage remains prudent, even following its largest acquisition to date (Wencor). The company is already deleveraging and returning toward historical norms.

🔹 Valuation Metrics: Share Price (HEI): $320 | P/FCF: ~42x | EV/EBITDA: ~32x

On traditional multiples, HEICO looks pricey. But when adjusted for:

Durable mid-to-high single-digit organic growth and mid-single digit inorganic growth

High reinvestment rates (>100% of FCF conversion)

A 20+ year runway across niche aerospace and defense markets

Industry-leading capital allocation by the Mendelson family

…then perhaps that premium is deserved.

As Morningstar put it:

“In a sum-of-the-parts analysis or through scenario-based forecasting, Heico remains attractive.”

Even Berkshire Hathaway took notice, initiating a small position in 2024 with an estimated cost basis between $150–$180 (HEI.A shares).

A Quick Mental Framework to Estimate Potential Returns

Just like I explained with M&A driven Constellation Software spin-offs, 🔗 Topicus and 🔗 Lumine, Heico can appear expensive when viewed through traditional trailing multiples, but the real value lies in: Reinvestment rates, Free cash flow generation and Returns on Capital

🔹 Using Market Leonard’s preferred method

Mark Leonard’s preferred method for estimating shareholder returns (IRR) combines profitability and growth:

Shareholder IRR = ROIC + Organic Growth

(Source: Q1 2008 Conference Call & 📎 M. Leonard’s Letters Collection)

So, ahead of the full release of my Capital Efficiency and Growth models for Heico, here’s an early snapshot:

ROIC (adjusted NOPAT, divided by total invested capital inc. Goodwill) is estimated around ~12-15%

Add in ~5-7% long-term organic growth

➡️ That implies a 17–22% IRR, 19.5% IRR at the mid-point, over a full investment cycle—assuming capital discipline is maintained and the current Forward FCF multiple (~42x) holds steady.

If we were to assume a lower FCF multiple, closer to Heico’s historical multiple of 35x, —which I think is more reasonable— we would get to:

📌 Shareholder IRR = ROIC + Organic Growth ± Valuation Impact

With:

Where:

Ending P/FCF = Fair P/FCF at the end of the holding period

Current P/FCF = P/FCF at the time of purchase

N = Holding period (in years)

Heico’s case:

Forward P/FCF = 42x, well above its 5-year normalized average of 35x.

Assuming a 5-year holding period, a reasonable fair P/FCF might be 35x (considering its high quality and historically high multiple).

Using the formula above, this results in a valuation decrease of -3.7% per year

So, Heico’s expected returns over 5 years is:

ROIC + Organic Growth ± Valuation Impact ≈ 19.5% - 3.7% = +15.8% CAGR

Of course, this approach —although straightforward— doesn’t capture intrinsic value fully and it’s way oversimplified, so I like to complement it with my DCF and reversed-engineered DCF models.

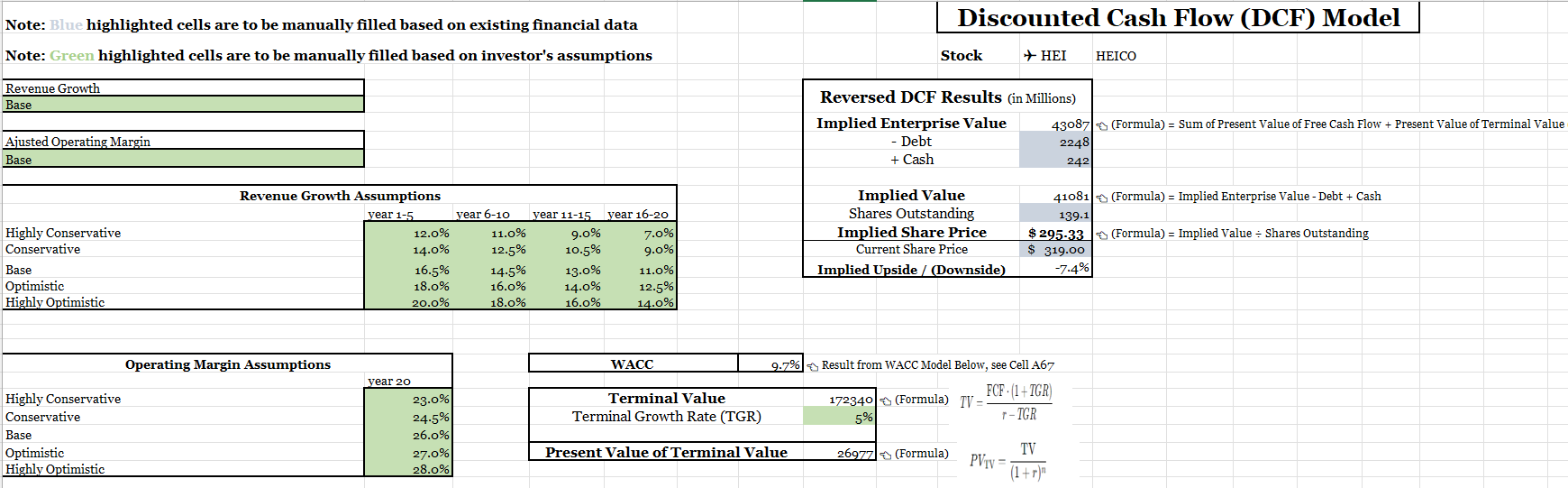

DCF Model Result (over a 20-year period)

Base case scenario assumptions:

Mix of inorganic growth (mid-single digits) driven by a mix of small and large acquisitions + organic growth (high-single digits) = 16.5% revs growth over next 5 years. From there, I get down to 14.5% revs growth on year 6-10, 13% growth on year 11-15 and finally 11% growth on year 16-20, before reaching a Terminal Value Growth of 5%.

Operating margins improve from the current 22.5% to 26% level over the next 20 years.

Cost of capital (WACC) estimated at 9.7%

This -7.4% implied downside was based on a $320 share price for HEI at the time of analysis. As discussed earlier (see the Fun Fact section), HEI.A shares offer better value with a 22% discount. However, due to the uncertainty around if or when this price gap may close, I’ve excluded it from the DCF model assumptions.

The results suggest Heico is fully priced at current levels in the short-term.

🔐 Reversed DCF Model (20-year horizon), Growth & Capital Efficiency Insights — Available for Paid Subscribers

The full Heico valuation suite—including the DCF and Reversed DCF models, Capital Efficiency model (ROIC, ROIIC, ROCE), and Growth Model (Reinvestment Rate × ROIIC to estimate intrinsic value growth)—is available for download in the Expanse Stocks 🔗 Portfolio corner.

Conclusion: A Niche Giant with a Long Runway

Heico isn't trying to be everything to everyone. In a sea of aerospace giants chasing innovation and scale, Heico has quietly carved out a niche dominant position by doing the opposite — embracing complexity, focus, and patience. It’s become the most trusted provider of critical components in high-stakes industries by staying disciplined and true to its niche.

With its large scale in PMAs, a consistent and disciplined M&A flywheel, a long-term family-led culture, and a proven record of capital allocation, Heico is, in my view, a textbook example of quiet, long-term compounding.

Yes, the stock looks expensive. But you're buying into a business with 50%+ PMA market share, decades of customer trust, a near-impossible-to-replicate approvals base, and ample room for future growth. So, the price might just be the cost of quality.

For investors looking for long-duration compounders in the industrials space, Heico is a rare breed.