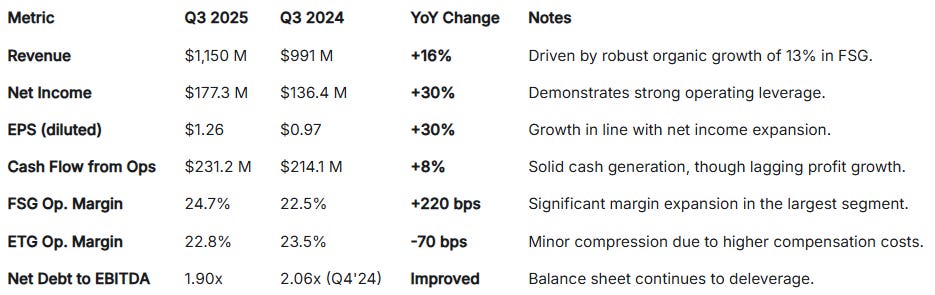

Heico delivered another quarter that showcases why this aerospace compounder deserves its premium valuation. Net sales grew 16% to $1.15 billion, and the group showed even better operating leverage with operating income up 22% and net income up 30% to $177.3 million, or $1.26 per share as the company's razor-and-blade model keeps firing on all cylinders.

Performance Drivers

1. Flight Support Group (FSG): The Growth Engine

The star of the show remains the FSG, which posted its twentieth consecutive quarter of sequential sales growth. Think about that for a moment: five straight years of growth in the commercial aerospace aftermarket, weathering everything from supply chain disruptions to post-pandemic recovery volatility.

The numbers:

Revenue grew 18% to $802.7 million. Contribution from 13% organic growth. This organic growth figure is particularly positive because it strips out the acquisition noise and shows the true demand strength in their core markets.

But what really caught my attention was their operating income growing 29% to $198.3 million. That's serious operating leverage, with margins expanding from 22.5% to 24.7%. When you're selling aftermarket parts to airlines with a growing number of old fleets that need their planes flying, pricing power shows up in exactly this way.

2. Electronic Technologies Group (ETG): Solid 10% Growth with Margin Pressure

The ETG delivered but its profitability story was more subdued.

Revenue increased 10% to a record $364.5 million, with 3% contributions from acquisitions and a 7% increase in organic sales.

Operating Margin compressed to 22.8% from 23.5%. Management attributed this decline to an increase in performance-based compensation expenses, probably higher bonus accruals.

Profitability Paired with Lower Cash Flow Conversion

Unlike companies where GAAP earnings can be misleading, Heico's reported profit closely reflects its operational performance. The 30% increase in net income was driven not only by higher sales volumes but, more importantly, by substantial margin expansion within the larger FSG segment.

Cash generation was okay, with Cash Flow from Operations up 8% to $231.2 million. The slower growth versus net income was largely due to a sizable increase in Net Working Capital. While cash flow conversion bears watching, I’m not overly concerned given management’s strong track record in capital allocation.

The Capital Allocation Story

What stands out most about Heico is its ability to absorb the large Wencor acquisition while still deleveraging. Over the past nine months, Net Debt to EBITDA improved from 2.06x to 1.90x, giving them firepower for their next wave of acquisitions.

This is textbook disciplined capital allocation, funding growth without overextending leverage, while generating enough cash to simultaneously reduce debt.

The Aerospace Aftermarket Thesis Intact

These results reinforce why I remain bullish on the aerospace aftermarket thesis. Once airlines commit to specific aircraft platforms, they’re locked into the parts ecosystem for decades. Heico’s FSG capitalizes on this dynamic through its Parts Manufacturer Approval (PMA) business, producing FAA-approved alternatives to OEM parts at superior margins. I broke this down in detail in my recent Heico investment thesis: 🔗 Deep Dive Brief: Heico

FSG’s twenty consecutive quarters of growth shows the resilience of aftermarket demand. Airlines may delay new aircraft purchases during downturns, but they can’t defer maintenance on their existing fleets.

What to Watch Going Forward

Key metrics I’m tracking are straightforward:

FSG organic growth sustainability: Can they maintain double-digit organic growth as comps get tougher?

Acquisition pipeline execution: With leverage improved, they have room to reaccelerate M&A following the Wencor acquisition in 2023.

ETG margin trajectory: Is the compensation-driven margin pressure temporary, or does it show something more structural? Ideally, this segment sustains low double-digit growth.

Aerospace recovery cycles tend to be long and durable once underway, and we may still be in the early innings of post-pandemic normalization.

Valuation Context

At current levels, Heico trades at premium multiples that clearly reflect its quality and growth (47x FCF NTM and 31x EBITDA). The 30% net income and EPS growth this quarter shows why investors are willing to pay up, even Buffett picked up shares in Q2 2025. When the model works, the operating leverage is substantial.

In my view, businesses with genuine moats in expanding end markets deserve premium valuations. Heico’s combination of aftermarket defensibility, disciplined M&A, and best-in-class capital allocation places it in that camp.

You won’t get it cheap. But if the stock dips, I’d better be ready. Quality compounders rarely stay discounted for long.

Thanks for following along,

—Nikotes

Unlock Premium Content – For just $0.39/day ($12/month) or $0.27/day ($100/year)!

🔗 Full Portfolio Content - 🗓️ Monthly Updates (Last Update: 30-Nov-2025)