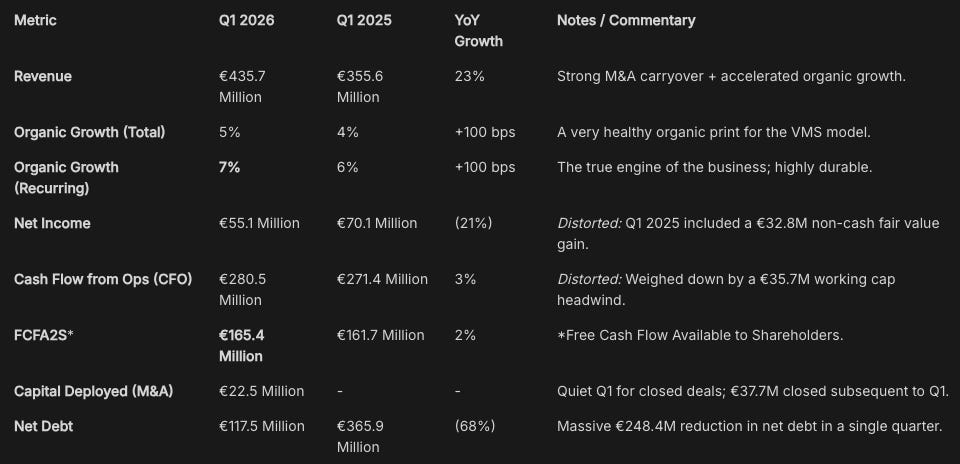

Topicus reported Q1 2026 earnings yesterday, and I suspect many investors looking at the headline numbers walked away confused, if not outright disappointed.

Net income down 21%.

Operating cash flow (OCF) growth of just 3%.

M&A deployment that looks muted and sluggish.

For a company that grew revenue 23%, that’s a lot of apparent contradiction packed into a single quarter.

The thing is almost none of it is really representative of Topicus’ financial health and long-term trend.

Let me walk through what I think actually happened this quarter and why I believe the underlying business is in better shape than the reported numbers suggest.

Financial Results

The accounting noise, aka the Asseco Poland noise

Before anything else, we need to address the 21% decline in GAAP Net Income head-on, because if we don’t, everything else becomes harder to interpret.

In Q1 2025, Topicus acquired its initial stake in Asseco Poland and was carrying it at Fair Value (FVOCI). This generated a €32.8 million mark-to-market paper gain that flowed directly into the income statement.

That gain does not repeat in Q1 2026 because the investment has since been moved to the equity accounting method. Once you strip that one-time Q1 2025 gain out of the comparison, underlying operational net income didn’t decline 21%, it actually grew approximately 48% YoY. A 21% decline that is in reality a 48% increase. Not bad, don’t you think?

Now that Asseco is on the equity method, a different (and equally important) accounting mechanic kicks in. Stay with me:

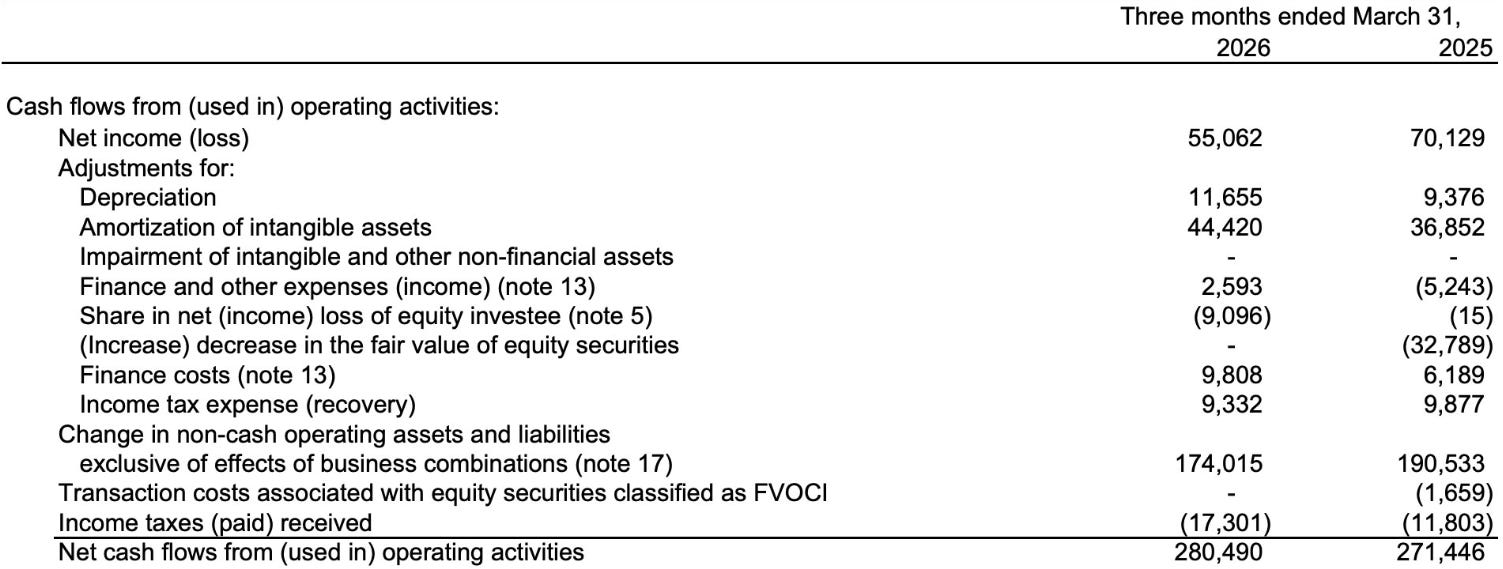

(1) Topicus’s 23.14% proportional share of Asseco’s net income — €9.1 million in Q1 2026, reflecting Asseco’s Q4 2025 performance due to the three-month reporting lag — flows into Topicus’s P&L below operating income. This is pure paper income. It hits the income statement, but because no cash was received, it gets backed out entirely in the non-cash adjustments section of the cash flow statement.

(2) Topicus only receives actual cash from Asseco through dividends, and no dividend was paid during the quarter.

Investors who do not understand this will systematically misread both the income statement and the cash flow statement every single quarter going forward. I don’t blame them… it’s messy. Hopefully, this will smooth out over time.

Why the “muted” cash flow growth is not what it appears

Q1 is structurally Topicus’s most powerful cash generation quarter. The company collects annual software maintenance fees upfront in January, creates a large deferred revenue balance, and then bleeds that balance down over the remaining three quarters as revenue is recognized. The result is a predictable cash geyser at the start of each year.

So, what happened in Q1 2026 ?

This quarter, Topicus generated €280.5 million in operating cash flow vs €271.4 million a year ago. A 3% operating cash flow growth against a 23% revenue growth deserves a proper explanation rather than dismissal. Two items explain virtually the entire gap, and neither reflects anything about the underlying earnings power of the business.

(1) Working capital fluctuations and accounts payable timing. (line 7)

In Q1 2025, Topicus delayed payments in a way that created a +€31.8 million tailwind to reported cash flow. In Q1 2026, that reversed, creating a (€3.9 million) headwind. The YoY swing is approximately €35.7 million. A comparison problem, not an operational one.

(2) Old, shitty cash taxes (last line)

They increased by €5.5 million YoY (€17.3 million vs. €11.8 million), partially a function of the company’s growing profitability.

Normalize for just these two items and Q1 2026 operating cash flow growth comes out around 18%, which maps better with the reported 20% expense growth and 23% revenue growth this quarter. All this to say the cash conversion engine is not broken.

The “great deleveraging” quarter and what it means for the rest of 2026

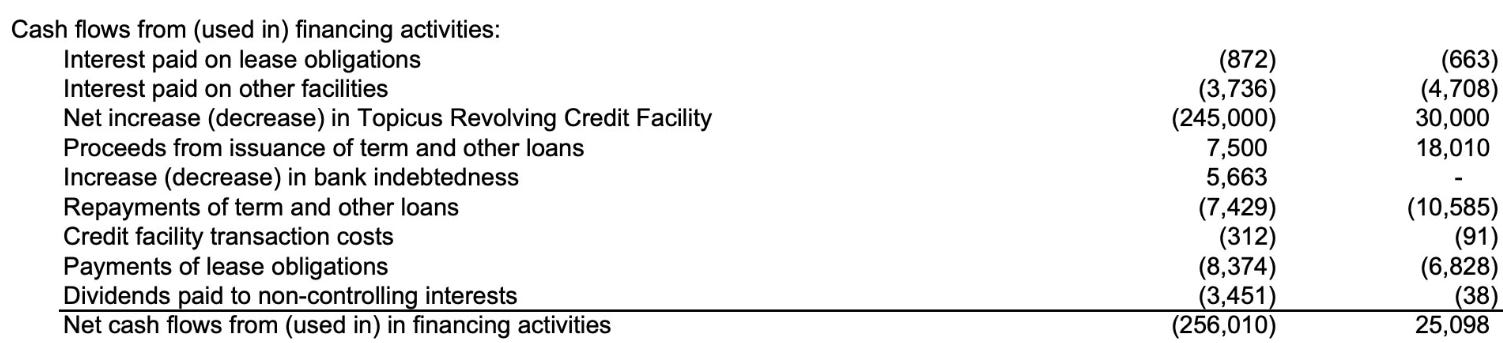

So how did Topicus use that “muted” operating cash flow this quarter? Like the best serial acquirers do: with conviction.

Management paid down €245.0 million of the revolving credit facility in three months (line 3 below), wiping out the majority of the debt taken on to fund the Asseco investment last year.

Total debt fell from €692.5 million at year-end to €448.6 million by March 31, 2026. With €331.2 million in cash on the balance sheet, net debt sits at nearly €117.5 million.

To put that in context: the company generated €165.4 million in FCFA2S in a single quarter, and it is now carrying less than one quarter’s worth of FCFA2S in net debt. The balance sheet, which was one possible source of investor anxiety heading into 2026 after that huge 2025 M&A spree, has essentially been rebuilt in a single quarter. Topicus enters the remainder of the year with a coiled spring.

The organic growth story is the one that matters most, particularly in this market

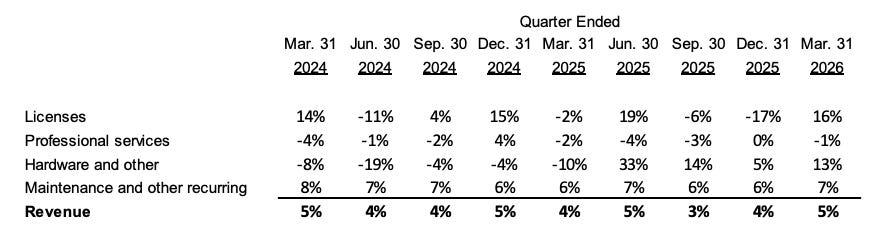

The number I keep coming back to is 7% organic growth in maintenance and other recurring revenues. This matters for a few reasons.

Maintenance revenue is 73% of total revenue. It is the most predictable, highest-margin segment. It is the line item that “SaaS-mageddonistas” bears will point to when making the case that AI is beginning to structurally erode VMS’s pricing power or retention. And it is growing at 7% organically.

There is zero evidence of AI-driven churn in these numbers. What we are seeing instead is the opposite: Inflation-linked pricing increases flowing through, module upsells layering on top of the base, and customers remaining as locked in as ever to mission-critical software that runs their operations.

It would frankly be strange to expect anything different from software that handles payroll for municipalities or case management for healthcare systems, but the market has spent the better part of 1-2 years convincing itself that even this category of software is terminally threatened. The Q1 numbers do not support that narrative.

Overall organic growth came in at 5%, and when you combine that with 23% total top-line growth (the remainder coming from M&A carryover), the picture is a company executing across both its organic and inorganic engines simultaneously.

The M&A pipeline: Slow start, the PEMS strategy getting validated

Q1 2026 was quiet on M&A, with €22.5 million in total consideration deployed. I am not particularly concerned by this, though I understand why some investors flag it given the monstrous balance sheet capacity now available.

My observation is that public SaaS multiples have been decimated over the past 12 months, but private market valuations have not followed, yet. Private markets (less exposed to panic / euphoria) lags public, both on the way up and the way down, because the volatility simply isn’t present.

My expectation is that as mid-market private equity fatigue sets in through 2026, the bid-ask gap narrows and Topicus hits the accelerator. Management has already deployed an additional €37.7 million subsequent to quarter-end. Not that much either. It will be worth monitoring how the pipeline evolves in Q2 and going into Q3.

The other angle worth watching is the Constellation-style (or Topicus-style I should say) minority stake playbook. Constellation made a significant investment in SABRE in Q1, and Topicus’s own Asseco investment is validating the PEMS (Permanent Engaged Minority Shareholder) strategy as a viable and highly capital-efficient use of the balance sheet. I wouldn’t be surprised to see Topicus make another move in this direction soon. When you have the balance sheet they have today and private market valuations that haven’t budged, patient capital deployed into public minority positions seems like the way to go these days.

The Dutch tax dispute, the one minor risk to flag

There is one item I would not dismiss as accounting noise. The Dutch Tax Authorities are challenging the deductibility of Topicus’s employee bonus program for years 2016 through 2018 onwards. The company has not provisioned for this, and the potential liability currently stands at €8.4 million (up slightly from €8.0 million at year-end due to accruing interest). This is not balance-sheet-threatening at current scale, but it is a real, unresolved contingency that investors should track. It did not move meaningfully this quarter, but it remains an open item.

Putting it together

The headline read on this quarter (declining net income, sluggish cash flow growth, low M&A deployment, etc.) is almost entirely a function of accounting mechanics and YoY timing comparisons that have nothing to do with the underlying business.

The actual read is: 5% overall organic growth with 7% recurring revenue acceleration, a balance sheet that has been almost completely reset in a single quarter, a cash conversion engine running at roughly 18% normalized growth, and a PEMS strategy that is beginning to generate real equity income contributions.

I don’t think the market has fully processed the Asseco accounting reversal yet, which created exactly the kind of messy optics that compress multiple for companies like Topicus. Q1 2026 strips a lot of that noise away when you dig deeper.

What’s left is a company with accelerating organic growth, exceptional liquidity, and a runway primed to reaccelerate M&A through the back half of the year (hopefully).

So, while Topicus’ valuation has been compressed over the last year; the fundamental picture is not.

Thanks for following along,

— Nikotes

Unlock Premium Content – For just $0.39/day ($12/month) or $0.27/day ($100/year)!

🔗 Portfolio Corner - 🗓️ Monthly Updates (Last Update: 3-May-2026)

Great article! Thanks

PEMS strategy = equity method accounting = only dividends from the holding is included in the calculation of FCFA2S, nothing else. The company needs to find a way to include the real value (should be a % of FCF or just operating income of the minority stake). Otherwise, if the minority stake does not pay dividends, the value is not reflected in FCFA2S at all.