Mercado Libre Q4 2025

Trading Margins for Market Dominance. But Is it a Good Strategy At This Point?

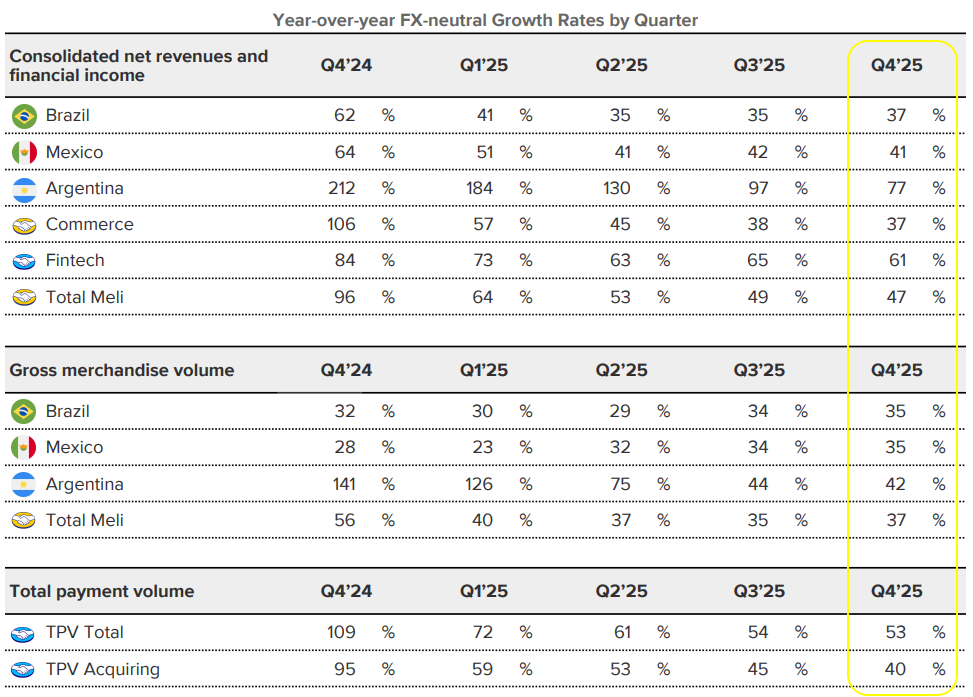

Mercado Libre reported Q4 2025 earnings that perfectly encapsulate, once again, why this company remains one of the most compelling growth stories in public markets. The headline numbers: 45% revenue growth to $8.8 billion, but operating margins compressed 340 basis points to 10.1%.

The market's initial reaction to the margin compression is, once again, predictable … *sigh* ... but misguided. Let me explain why.

Financial Results

Big Numbers At Bigger Scale

A Margin Compression “Problem”

Operating income grew 22% YoY, but margins fell from 13.5% to 10.1%. Before anyone panics, CFO Martin de Los Santos was explicit about what’s happening here:

“We estimate the combined impact of our strategic investments... which include the lower free shipping threshold in Brazil, CBT [Cross-Border Trade], 1P and the credit card, was equivalent to 5-6 percentage points of operating margin in Q4’25.”

“We are not managing the business for short-term margin... We will not hesitate to invest in order to capture those opportunities as we have done in the past, even if that puts some short-term margin pressure... We believe these investments are creating a foundation for future growth.”

— Martin de Los Santos, CFO

“We are not managing the business for short-term margin.” This quote sound tired, at least to the market, but management estimates that strategic investments in shipping subsidies, credit cards, first-party inventory, and cross-border trade are dragging margins by 5-6 percentage points.

In my view, this isn’t margin compression in the way investors should worry about. MELI isn’t seeing margins collapse because its core economics are deteriorating. It’s choosing to deploy capital aggressively across logistics, fintech, and inventory to deepen its moat while the opportunity set is still wide open.

The company is making a bet that owning the user now will generate significantly higher returns over the next decade than optimizing for today’s margin profile.

The unit economics tell you everything you need to know about whether this strategy is working. Despite flooding Brazil with lower-ticket items (which should theoretically pressure unit economics), shipping costs per unit fell 11% YoY. That’s the entire story right there: MELI is subsidizing shipping to win volume, but their logistics network is efficient enough that the actual cost of moving each additional item is declining. This is what operating leverage looks like before it shows up in the P&L.

The R$19 Effect: Brazil Commerce Acceleration

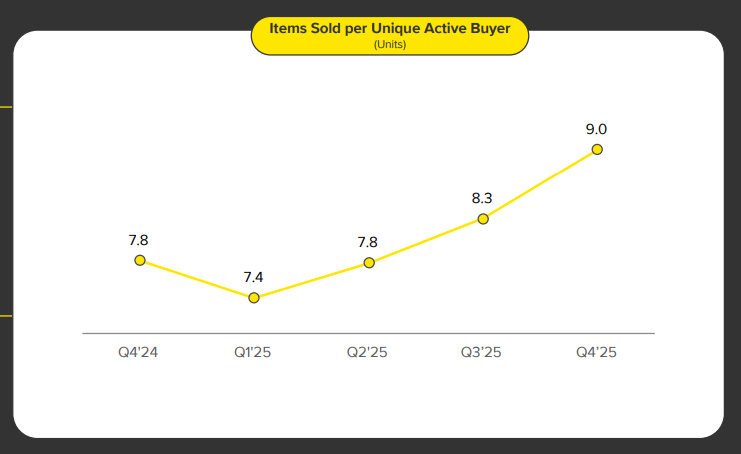

The decision to lower Brazil’s free shipping threshold from R$79 to R$19 has been a key driver of growth. Items sold in Brazil accelerated from 26% growth in Q2 to 45% in Q4.

"New buyers that have come to Mercado Libre since June when we launched the new value prop are buying more items across a larger number of categories with higher retention rates compared to cohorts of new buyers prior to that change." — Ariel Szarfsztejn, CEO

New buyer cohorts are showing higher retention and broader category engagement, which shows MELI is successfully training a new generation of Latin American consumers to shop online first.

With 45% volume growth in Brazil, MELI is almost certainly taking significant share from both Asian cross-border players (Shein, Shopee) and local incumbents (Magazine Luiza, Casas Bahia). The heavy logistics Capex of the past few years is now validating itself through competitive positioning that rivals simply cannot match.

Fintech: From Payments Processor to Primary Bank

Mercado Pago continues to be the most underappreciated part of the MELI story.

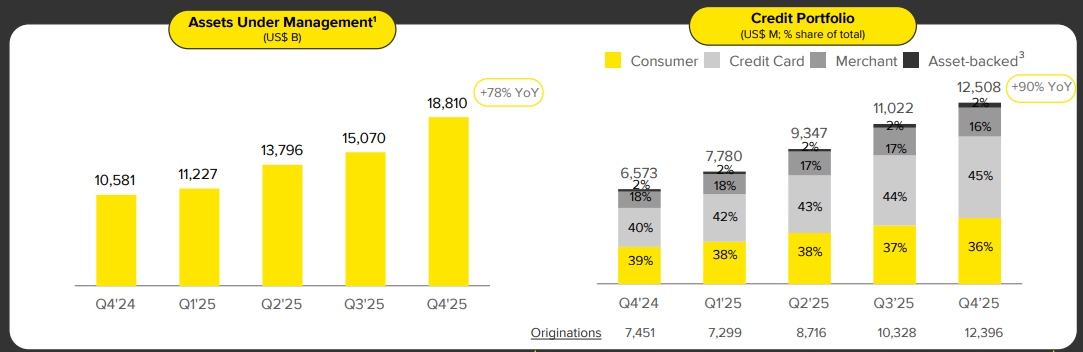

Assets Under Management grew 78% YoY, driven by interest-bearing accounts. This matters because MELI is starting to fund its massive credit expansion (credit portfolio up 90% to $12.5 billion) with customer deposits rather than wholesale funding. This is how you build a bank, not just a payments rail.

The credit card portfolio is the primary growth driver here, and the unit economics are proving out faster than expected.

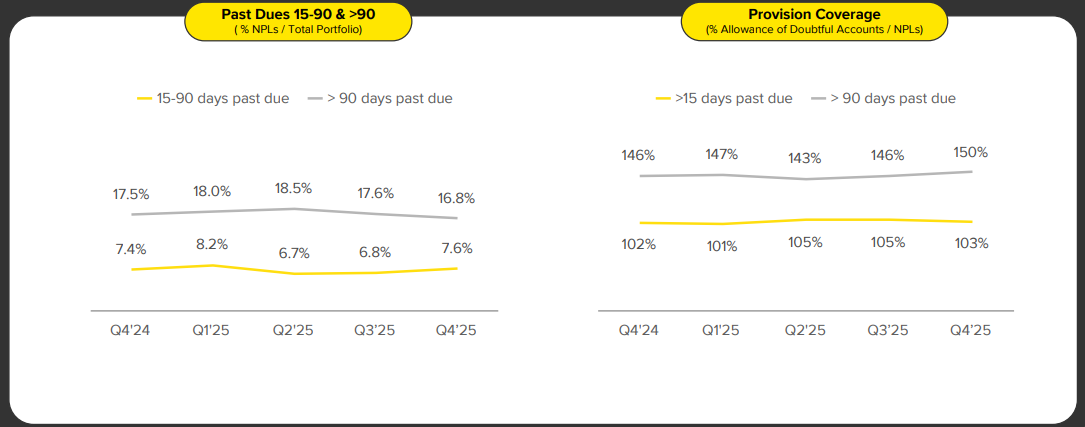

Management noted that credit card cohorts in Brazil reach NIMAL breakeven (profitability after losses) in 12-18 months, and 75% of the Brazil card portfolio has already hit this milestone. For context, NIMAL expanded to 23.3% from 21% despite the rapid portfolio growth, which tells you the company is pricing risk correctly.

"More important than NPLs are Net Interest Margin After Losses and those improved... Therefore, what we did was we increased the number of people and the riskier number of people we give credit to, but we price that risk accordingly. And therefore, we ended up having a significantly larger spread than we did on the prior quarter. So I think this was a calculated risk and it worked out well."

"Cohorts that are older than 2 years are already profitable at a NIMAL level... half of the portfolio is already NIMAL [positive] in Brazil."

— Osvaldo Giménez, Fintech President

There will be noise around early-stage delinquencies (15-90 days) ticking up.

But, as Fintech President Giménez explained, they’re deliberately expanding down the credit curve and pricing that risk accordingly. The wider spread (NIMAL) is the reward for taking that risk. This is textbook subprime lending done correctly: price for the risk, accept higher delinquencies, and make sure your net return is attractive.

The Flywheel in Full Display

This quarter perfectly demonstrated (once again) why MELI’s ecosystem is so powerful.

The commerce investments (shipping subsidies) drove traffic. That traffic fueled the advertising business, which grew 67% YoY. The data from that traffic enabled massive credit issuance, which grew 90%. And the credit cards drive “principality” in Fintech, with users making Mercado Pago their primary financial account which closes the loop by driving more commerce volume. The flywheel in full display.

Each piece reinforces the others. This is why MELI can sustain 40%+ growth at $8.8 billion in quarterly revenue, a scale where most companies are happy with mid-teens growth.

AI: Tailwind, Not Headwind

New CEO Ariel Szarfsztejn addressed the “Agentic Commerce” question head-on, the fear that AI shopping agents might commoditize marketplaces by making product discovery platform-agnostic. His response was simple: MELI will build the best agent because it has the best first-party data on Latin American consumer behavior.

"We are betting and putting our efforts on what we can control, which is building the best assistant possible... relying on our first-party data to create the best search, recommendation, and discovery engine... I think that MercadoLibre is well-positioned to capture this technology transformation, which... will accelerate the migration from offline retail into online retail." — Ariel Szarfsztejn, CEO

Far from being disrupted, MELI is using AI as an accelerant. The 67% growth in advertising revenue is partially AI-driven (better targeting, higher ad loads), and credit underwriting is becoming more precise as AI models ingest more data. MELI controls the data layer in Latin America’s two most important digital businesses (commerce and fintech), which makes it exceptionally well-positioned in an AI-driven future.

What to Watch: A Path Back to Margin Expansion

Management made clear that 2026 will see continued aggressive investment. The market needs to accept that ~10% operating margins are the new baseline for the next 12-18 months. The critical question is whether the 5-6 percentage point investment drag eventually converts into operating leverage as volume scales and logistics efficiency improves.

The early signs are encouraging. Unit shipping costs fell 11% despite lower average order values, and credit card cohorts are breaking even faster than expected. If these trends continue, we should start seeing margin expansion in late 2026 or 2027 as the investment cycle normalizes and operating leverage kicks in.

Here’s what I’ll be monitoring:

Direct Contribution Margin in Brazil: Watch whether logistics efficiencies begin offsetting shipping subsidies in the next few quarters

NPLs >90 days: Early delinquencies are expected given the credit expansion, but late-stage delinquencies are where real credit losses show up

NIMAL trajectory: If this continues expanding while the portfolio grows, it confirms the risk-adjusted pricing is working

The Investment Case

MELI is executing a playbook that few companies have the courage to run: sacrifice near-term margins to dominate emerging markets before they fully mature. The difference between MELI and companies that blow up doing this is that MELI’s unit economics are actually improving while margins compress. That’s the entire difference between intelligent capital allocation and reckless growth spending.

The reality is that MELI is the only company in Latin America successfully building both a dominant e-commerce platform and a scaled fintech business. That combination is rare globally and essentially impossible to replicate at this point in LatAm. The moat isn’t just the logistics network or the credit models, it’s the data flywheel that connects them.

Investors need to decide whether they’re willing to accept 10% operating margins today in exchange for owning the digital infrastructure of Latin America’s consumer economy. The items sold acceleration (+45%) and the credit portfolio growth (+90%) tell you MELI is winning the user. The falling unit costs tell you the economics work. The margin compression is the price of admission to capture this opportunity before the market fully consolidates.

If you’re uncomfortable with MELI’s margin profile today, you probably don’t understand what management is building. This isn’t margin compression from competitive pressure (at least not in any material way) or structural deterioration, this is margin investment to cement a two-decade competitive advantage. There’s a meaningful difference between the two, and mistaking one for the other is how you miss great companies at inflection points.

Thanks for following along,

—Nikotes

Unlock Premium Content – For just $0.39/day ($12/month) or $0.27/day ($100/year)!

🔗 Portfolio Corner - 🗓️ Monthly Updates (Last Update: 30-Jan-2026)

Increasing my position today FYI.