Lumine reported Q1 2026 results this week, and the market didn’t really know what to do with them.

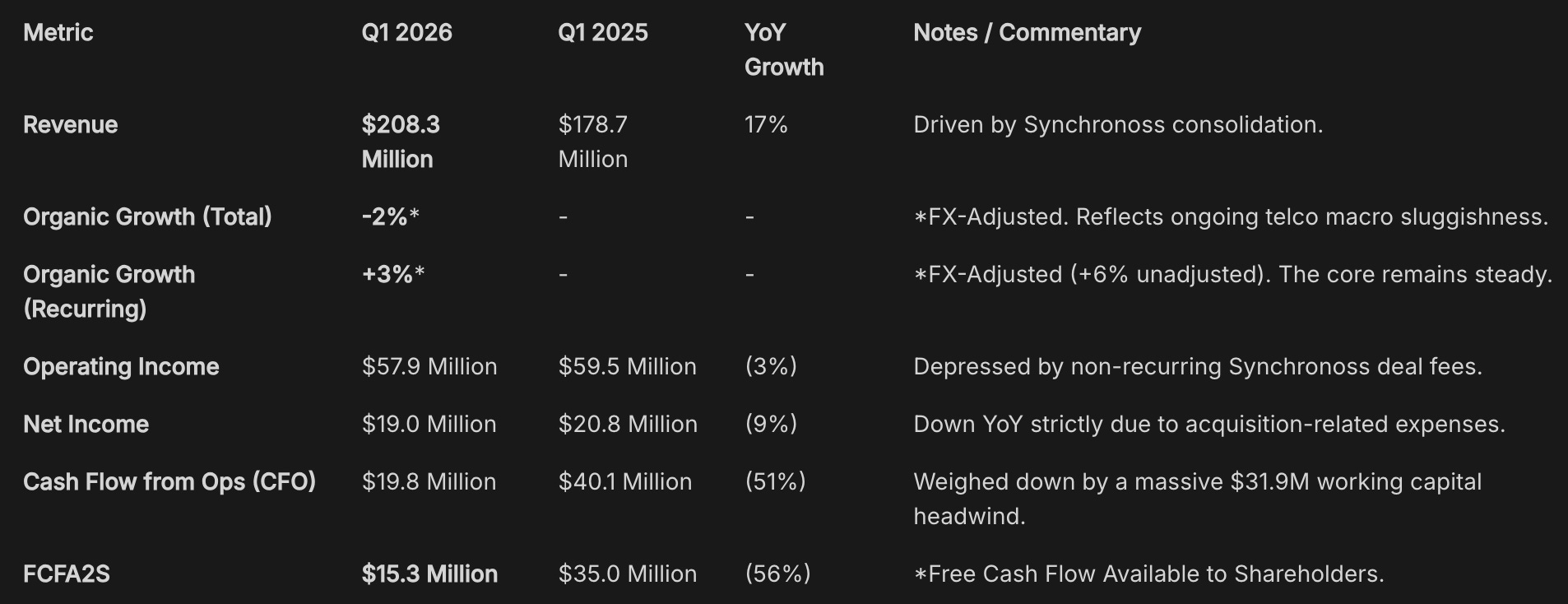

The headline numbers weren’t pretty: free cash flow down 56% YoY, organic growth at -2%. On the surface, not the cleanest quarter Lumine has reported lately.

And yet, if you read beyond the first two lines of the press release, there’s arguably more to like than dislike here. I suspect most won’t, which is why I want to go through this in some detail.

Let me be upfront about my expectations going in: I never thought this quarter would look pretty on the surface. Lumine closed the $306.7 million acquisition of Synchronoss Technologies on February 13th, meaning Q1 only captured roughly six weeks of a massive, messy, formerly public-company integration. Anyone expecting a quarter like this to look pristine was never paying attention to how the Constellation playbook works.

dre1012 (X account) summarized the market’s reaction to the messy Lumine / Topicus prints pretty well this week 🎯

Let’s add some context to the numbers for shareholders focused a bit too much on the short term 👀

Financial Results

Deconstructing Organic Growth

A -2% FX-adjusted organic growth rate sounds bad in isolation. Once you break it apart, it’s actually telling a more encouraging story.

The drag came entirely from two revenue lines: hardware (-59% FX-adjusted organic) and licenses (-13%). In the VMS roll-up model, hardware is low-margin, capital-consumptive, and unpredictable. There is nothing really strategic about it. Shrinking hardware revenue on purpose while maintaining core software recurring revenue is what a disciplined operator like Lumine should be doing. I don’t think enough people understand that in this model, revenue quality matters far more than revenue quantity.

And the core is holding up. Maintenance and other recurring revenue (the recurring high-margin lifeblood) grew 27% reported to $160.2 million, now accounting for 77% of total revenue, up from 70% a year ago.

FX-adjusted organic growth for this line came in at +3% (+6% un-adjusted). That might sound modest, but consider the context: we’re talking about mission-critical telecom software in a global environment where carrier budgets are being squeezed almost universally. The fact that Lumine is retaining customers and passing through Inflation-linked price increases at all tells you how embedded this software actually is.

Nobody is ripping out a mission-critical billing or network management system to save a few points of margin. Put -2% headline organic growth alongside +3% FX-adjusted recurring growth, and the picture changes.

The Synchronoss Opportunity: Reading the Expense Lines

Operating income fell 3% YoY to $57.9 million resulting in margin compression, and FCFA2S dropped 56% to $15.3 million. Both of these numbers look bad but are temporarily misleading.

When you acquire a formerly public company, you inherit its full cost structure from day one. Synchronoss has spent years building overhead that “made sense” when you had to satisfy public market investors every 90 days: board fees, D&O insurance, compliance infrastructure, bloated executive compensation, and the general bureaucratic drag that comes with being a listed entity. Lumine has no interest in keeping any of it.

The Q1 expense lines are less a source of concern and more a precise roadmap for where margin recovery will come from over the next two to three quarters.

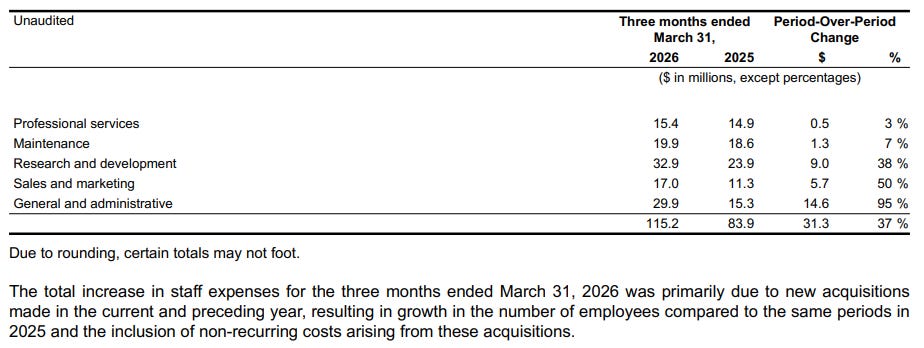

(1) “The total increase in staff expenses… was primary due to new acquisitions made in the current and preceding year”

(2) “The total increase in staff expenses… was primary due to new acquisitions made in the current and preceding year”

(3) …

G&A expenses grew 95% YoY to $29.9 million. This number alone tells you almost everything you need to know about the nature of the opportunity ahead for Lumine.

Sales & Marketing grew 50% to $17.0 million, possibly reflecting Synchronoss’s legacy habit of going after new logos rather than farming the installed base, the exact opposite of what Lumine’s operating model calls for.

R&D grew 38% to $32.9 million, likely bloated with non-core development that will be either pruned or shifted to lower-cost geographies.

I would even go as far as to say that if Q1 had not shown this kind of cost bloat, I would have been far more worried, it would mean Synchronoss was already running lean and there was little margin expansion left to capture.

So, does the Lumine’s margin compression in Q1 look structural to you?

It is the predictable result of consolidating roughly six weeks of a legacy cost structure that Lumine’s management team is now systematically dismantling. So, if history is any guide, expect operating margins to recover meaningfully in Q3 and Q4 as those levers get pulled. Mark it.

Capital Allocation Done Right

Another important thing that happened in this quarter did not show up in the income statement. It showed up in a footnote.

To fund the Synchronoss acquisition, Lumine drew $160 million on its corporate-level revolving credit facility. But the 🔗 Q1 2026 MD&A’s subsequent events section (look for “Synchronoss Term Loan and Facility”) shows something pretty interesting: on May 1st, 2026, Synchronoss secured its own standalone $110 million term loan and $10 million revolver at the subsidiary level.

This is the Constellation playbook executed, once again, to the letter.

By pushing the debt down to the subsidiary, secured by Synchronoss’s own assets, Lumine ring-fences corporate from risk. The subsidiary’s term loan proceeds likely flow back up to Lumine as a dividend or intercompany repayment, effectively retiring the corporate facility draw and reloading the centralized balance sheet. Lumine’s corporate revolver, recently extended to June 2029 with a $360 million capacity, is now largely available again, sitting alongside $248.2 million in cash.

Lumine didn’t use this acquisition to weaken its capital position. It used it to demonstrate, once again, that it can absorb a $300+ million deal and come out the other side fully loaded for the next one.

Now let’s dig into the cash flow decline as it deserves some context too.

Operating cash flow was dragged by a $31.9 million negative swing in working capital, explicitly tied to inheriting Synchronoss’s receivables cycle on consolidation.

That cash isn’t gone. It’s sitting in newly acquired receivables that will likely convert to free cash flow over the coming quarters. Anyone screening this quarter on trailing FCF and calling it a structural deterioration is making an analytical mistake.

The Risks

Now, I want to be honest about the risks here, because acknowledging them is also what allows you to hold conviction through the noise if you are an investor.

The Synchronoss integration is one of the largest and, possibly, most complex turnaround Lumine has attempted. If the cost-cutting, particularly the aggressive reductions in G&A and S&M, triggers unexpected customer churn or causes key engineering talent to exit before the software is stabilized, the subsidiary-level debt load becomes a real burden. This is always the risk in an aggressive public-to-private takeout. So far, management has shown no sign of mishandling this, on the contrary, but it bears watching over the next quarters.

The telecom software market is unlikely to become a tailwind anytime soon. Lumine itself acknowledges that its customers take a “long view to procurement decisions.” Organic growth in the -2% to +2% range is probably the realistic base case for the foreseeable future. If your investment thesis requires a reacceleration of organic growth, this might not be the right vehicle. If your thesis is built on capital allocation, margin expansion, and inorganic compounding (which is the right way to think about Lumine) then the current environment is largely irrelevant.

What Q1 Tells Us

Let me sum up what I think this quarter validated:

The core recurring software business is intact. +3% FX-adjusted organic growth in maintenance revenue, in this telecom environment, confirms that customer retention remains high and pricing is working.

The hardware and license run-off is intentional and structurally beneficial. Lower-quality revenue is being replaced by a higher-quality revenue mix. The 77% recurring revenue share is the highest it’s ever been.

The cost structure inherited from Synchronoss is visibly bloated and actionable. G&A +95%, S&M +50%, R&D +38% → these are primed optimization opportunities post-Synchronoss acquisiton, and Lumine’s management has already started addressing.

The balance sheet engineering is exactly what long-term shareholders should want to see. The subsidiary-level refinancing reloads the corporate revolver without equity dilution and keeps the M&A pipeline fully open.

The FCF decline is a timing and accounting artifact. Working capital absorption on a $300M+ acquisition is entirely normal and will likely reverse.

The optical read of this quarter : negative organic growth, collapsing free cash flow, margin compression,… It is the kind of noise that shakes out short-term investors and creates entry points (especially after a ~60% drawdown from the highs even before the Q1 release 😅) for those willing to look one layer deeper.

I don’t know many small-cap businesses that can close one of the largest acquisition in their history, inherit the full cost structure of a formerly public company, and still report positive operating income and growing recurring revenue (+27% YoY) in the same quarter. Lumine just did.

So it begs the question: Is the market getting lazier (and dumber) at analyzing serial acquirers?

I’d argue Constellation and Topicus are structurally more complex. Lumine is simpler.

Post-carve-out “shenanigans” are nothing new. Maybe this just reflects today’s market regime: momentum chasing AI winners (semis, etc.) while software gets relentlessly repriced under SaaS-mageddon.

Thanks for following along,

— Nikotes

Unlock Premium Content – For just $0.39/day ($12/month) or $0.27/day ($100/year)!

🔗 Portfolio Corner - 🗓️ Monthly Updates (Last Update: 3-May-2026)