After Sir Leonard stepped down last year, the bear case was ready:

AI disruption

New CEO doubts: “No one can replace Leonard”

CSU management bringing back conference calls this quarter was a smart move.

The key investor question isn’t just about AI, at least not yet. It’s about capital allocation at scale: How do you deploy billions annually while maintaining 20%+ IRRs?

CSU’s answer: PEMS — Permanent Engaged Minority Shareholder strategy.

A structure to scale capital deployment without diluting hurdle rates. And the 🧙♂️ is still there, guiding M. Miller & co. from the back seat.

Music to my ears. It shows CSU understands the laws of large numbers better than anyone and has a plan to evolve its playbook for the next phase.

Financial Results

The Numbers (And Why They Don’t Tell the Full Story)

Revenue grew 18% to hit just over $3 billion for the quarter, reaccelerating from +16%, with 9% maintenance and recurring organic growth in Q4 (6% constant currency). Not too shabby.

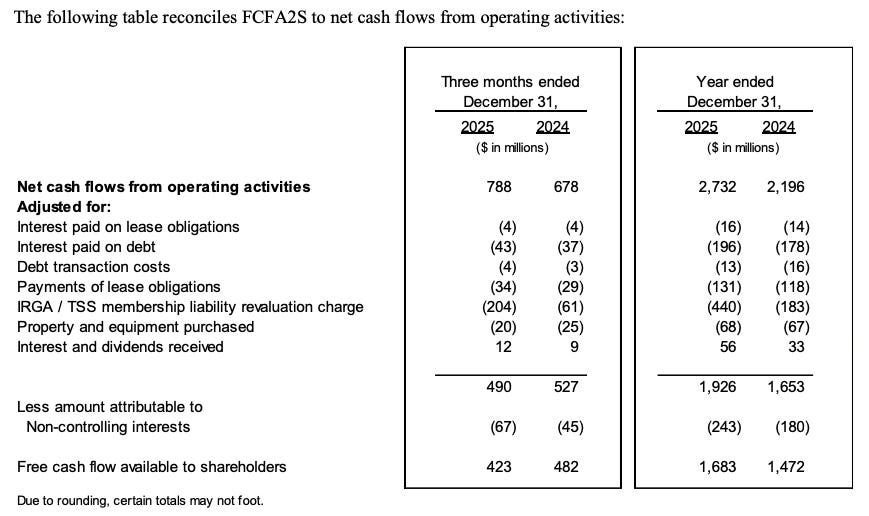

Another thing that stood out for some in the Fintwit / X community is that GAAP net income cratered 61% to $110 million and FCFA2S decreased by 16%.

The reality lies, once again, in the details: a $204 million non-cash revaluation charge related to CSU’s investment structures (specifically the IRGA/TSS membership liability tied to Asseco and Sygnity holdings).

This is pure accounting noise. Exclude the IRGA (as investors should) and the picture is clear:

FCFA2S +15.8% and +28.3% for the full year

Cash from Operations (CFO) +16% to $788M and full-year CFO at +24%

Focus on the true cash generation, not the GAAP earnings distorted by non-cash revaluations of CSU’s public holdings as they appreciate in value.

PEMS: The Strategic Response to Scale

The most significant development this quarter wasn’t in the financials at all. It was management’s formal articulation of the PEMS strategy, which has been quietly unfolding over the past few years with investments in companies like Asseco with Topicus leading the way, and now, CSI with Sabre.

On the new PEMS Strategy (Permanent Engaged Minority Shareholder) with Mark Leonard helping to craft it from the back seat:

We’ve also developed a new approach to deploying larger amounts of capital, what we’re calling a Permanent Engaged Minority Shareholder strategy or PEMS. Our investment in Sabre is the first meaningful expression of it. And I have to thank Mark Leonard who is helping us with this strategy and helped us explicitly on this particular investment. But the logic is straightforward. Permanent, meaning we’re long-term share -- long-term holders, not traders. We’ll work to ensure these companies endure as institutions. We’re engaged, which means we care about governance, management incentives and capital allocation, and we’ll actively work to have an influence where we think it creates value. Minority, we’re not acquiring these businesses outright. We want to partner with other shareholders, and we hope many of them become engaged long-term holders alongside us. — Mark Miller, President & COO

Here’s the problem CSU has been facing: at nearly CAD 64 billion in market cap, deploying $2-3 billion annually into small VMS acquisitions at 25%+ IRRs is becoming mathematically harder. The traditional playbook, buying $5-20 million revenue software companies from retiring founders at 3-5x EBITDA still works, but it can’t absorb all the cash CSU generates.

PEMS is management’s answer. Rather than trying to force-feed capital into overpriced small deals, they’re taking minority stakes in larger public companies, demanding board seats, and attempting to influence capital allocation and operational decisions. They’re essentially trying to export the CSU playbook to undervalued public companies without paying takeover premiums.

This is very clever, but it’s also an implicit admission that the classic model faces constraints at current scale. The thing is that being an engaged minority shareholder is fundamentally different from owning 100% of a business. You can advise, you can influence, but you can’t dictate. If management teams at portfolio companies like Sabre resist CSU’s governance suggestions, capital could get trapped in suboptimal investments.

Does that mean I’m less excited? Quite the opposite.

If executed well, this could become one of the most powerful levers available to them. With SaaS-mageddon leaving plenty of SaaS “cadavers” across public markets, it might create exactly the kind of hunting ground where an exceptional capital allocator like CSU can thrive.

The AI Question (And Why Management Gets It Right)

Let’s start this section with this quote on AI as a Moat vs. Table Stakes during the CC:

“I want to be direct about something, building products and features faster will not be what differentiates us long term. That capability will become widely available. It’s going to be table stakes. What will matter is what our businesses have spent many years developing, deep vertical knowledge, a genuine understanding of customer workflows... and the trusted relationships they’ve built.” — Mark Miller, President & COO

Management addressed the AI disruption narrative with a pragmatism that’s rare in today’s market. Mark Miller was explicit: AI-assisted coding will become table stakes, not a competitive advantage. Every software company will have developers using AI tools to write code faster.

What won’t be commoditized? Deep vertical knowledge, proprietary customer data, and entrenched workflows.

As I’ve been pointing at on different pieces released recently at Expanse Stocks, this is exactly where CSU’s moat actually lives. Miller’s vision of “knowledge networks”, using AI to mine CSU’s massive trove of customer-specific data to build better solutions, is the right way to think about this.

On Refusing to Centralize AI:

“As far as a large centralizing development or centralizing AI tools, we’re not really a big fan of that because... it means you’re taking away the ability for that business leader who could be in some country, somewhere... to move quickly to give them what they need... we’re very hesitant to centrally control anything here.” — Mark Miller, President & COO

The decentralized approach to AI adoption is also classic CSU. There’s no top-down mandate. Instead, hundreds of business units are experimenting, competing, and sharing best practices. The best ideas win and propagate organically.

While I find this reassuring, there’s still a tail risk worth acknowledging. If agentic AI eventually lowers the barrier to entry for bespoke vertical software over a 5-10 year horizon, it could pressure pricing power or increase churn. Management is confident this won’t happen, and their reasoning is sound.

Capital Allocation & The Buyback That Wasn’t

On Share Buybacks (NCIB):

“We have created a subcommittee within the Board to look at this... But at this point in time, we believe there are ample opportunities to deploy capital as opposed to buying back our shares.” — Jamal Baksh, CFO

CFO Jamal Baksh confirmed that the board evaluated implementing a share buyback program (!!) and ultimately rejected it.

The conclusion? There are still too many high-return opportunities available to justify buying CSU stock at current valuations.

In my view, that’s very good news. It suggests management continues to see attractive capital deployment opportunities and that buybacks simply don’t meet CSU’s self-imposed hurdle rates, targeting 20%+ IRRs.

In Q4 alone, the company deployed nearly $900M across traditional M&A and minority investments. Since year-end, in just a couple of months, they’ve already committed another $802M.

The capital deployment engine is clearly running hot, validating management’s decision to skip buybacks.

What This Means for Returns Going Forward

I’ve written before about the inevitable gravity of scale, and this quarter’s developments reinforce that thesis. CSU is no longer the CAD 10 billion market cap compounder it was a decade ago. At CAD 64 billion, the math changes.

The PEMS strategy is an intelligent adaptation, but it inherently carries different return characteristics than the classic VMS roll-up model. Minority stakes in public companies, even with board influence, are unlikely to generate the same 25-30% IRRs that buying private software companies at 3-5x EBITDA delivered historically.

Management confirmed that PEMS investments are evaluated using the same IRR hurdles as traditional acquisitions, which is reassuring. But the reality is that deploying billions annually while maintaining 20%+ returns is exceptionally challenging, regardless of strategy.

My base case remains that CSU will gradually see returns compress from the mid/high 20s toward the low twenties to high-teens over the next 5-10 years. This is just a graceful moderation driven by scale. Even at 17-22% IRRs, CSU would remain one of the best capital allocators in public markets.

What to Watch: The Numbers That Actually Matter

Here’s what I will be monitoring throughout the year:

Organic growth: Holding steady. No degradation despite AI fears. Management indicated this is a “good number for future organic growth”.

M&A volume: $571 million deployed in Q4 for traditional acquisitions, with the pipeline remaining full. Private market valuations haven’t contracted meaningfully, but CSU’s funnel of prospects is intact.

Free cash flow (exc. IRGA): Growing faster than revenue, which is what you want to see in a compounder. The $802 million in deals already committed for early 2026 shows the deployment pace isn’t slowing.

Thanks for following along,

—Nikotes

Unlock Premium Content – For just $0.39/day ($12/month) or $0.27/day ($100/year)!

🔗 Portfolio Corner - 🗓️ Monthly Updates (Last Update: 5-Mar-2026)

Thanks for writing and sharing!

Great article! Where do you see the FCF multiples going forward to be?