Constellation Software Q2 2025

A Perfect Example of Why GAAP Earnings Don't Tell the Whole Story and Why the Scale Question Remains

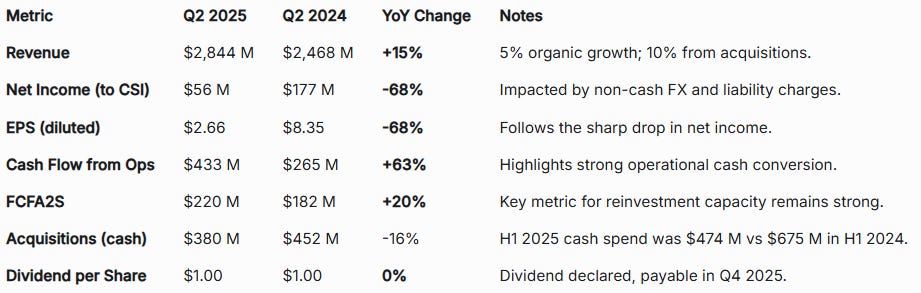

Constellation Software just delivered what I'd call a "textbook CSU quarter", one that shows really well why focusing on GAAP earnings for serial acquirers is a fool's errand. While reported EPS decreased 68% to $2.66, the underlying cash generation shows a different story.

The Numbers That Matter

Let me cut straight to what matters: Cash Flow from Operations surged 63% to $433 million, and Free Cash Flow Available to Shareholders grew 20% to $220 million. These are the metrics that determine CSU's ability to compound capital over the long term, and they're well on track with past performance but, at a higher scale.

Revenue growth of 15% was driven by the usual suspects, about 10% from acquisitions and 5% organic growth. The organic number is particularly encouraging, with maintenance and recurring revenue (now 75% of total revenue) growing 7%.

This is the sticky, predictable cash flow that makes CSU's acquisition model so powerful.

The GAAP Earnings Noise

The 68% decline in net income is almost entirely noise. Here's what happened:

Foreign exchange losses: $118 million vs. $4 million last year. This is primarily non-cash revaluation of foreign-denominated liabilities, i.e. FX headwinds.

IRGA/TSS liability revaluation: $126 million charge vs. $8 million last year, tied to Topicus performance. A revaluation that is non-cash but flows through P&L statement. This is a big one-off (or at least period-specific) expense.

Higher amortization expenses: $29 million increase from recent acquisitions.

These are exactly the types of non-cash accounting adjustments that make GAAP earnings misleading for understanding CSU's true economic performance. The thing is that none of these items affect the company's ability to generate cash or reinvest it profitably.

Why This Quarter Reinforces the Investment Thesis

What I find most compelling about these results is how they demonstrate CSU's operational resilience. Q2 is typically their weakest quarter for cash flow seasonality, yet they delivered exceptional cash generation relative to other quarters. This shows CSU’s portfolio businesses are performing well despite all the accounting noise.

The company's balance sheet remains fortress-like with $2.58 billion in cash and over $1 billion available in credit facilities. They've got more than enough dry powder to continue their acquisition spree, having already deployed $474 million in H1 and committed another $320 million post-quarter.

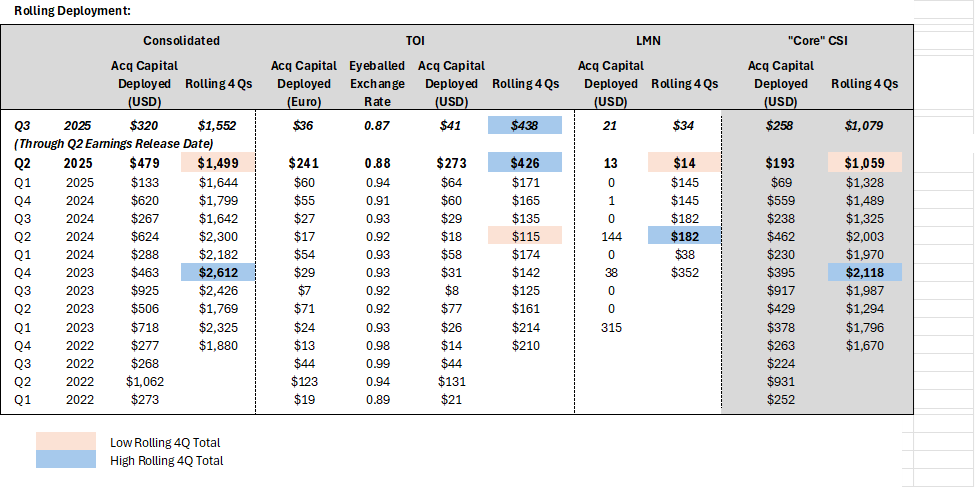

Borrowing a great chart from X user @wlep, which shows the rolling 4-quarter cash deployment into acquisitions for consolidated CSU, Core Constellation Software (CSI), and the spin-offs (TOI & LMN).

As you can see, despite a slow start to 2025, core CSI is beginning to pick up steam again while getting a solid boost from its spin-offs, particularly Topicus in recent quarters.

The Scale Question Remains

While these results are encouraging, they don't change the fundamental question many have been wrestling with: can CSU maintain its historical returns as scale increases?

The company deployed $380M in acquisition capital this quarter, down from $452M a year ago (-16% YoY). This could signal tougher market conditions and the growing challenge of sourcing attractive deals at their scale; or it might simply be a matter of timing, as acquisition opportunities rarely arrive in a straight line. Personally, I lean toward the latter explanation.

In any case, the reality is that as CSU continues to scale, it faces the unavoidable mathematical constraints of large-scale capital deployment. Even with robust cash flow growth, sustaining 20%+ IRRs on an ever-expanding capital base becomes progressively harder.

What to Watch Going Forward

I'm focused on two key metrics:

FCFA2S growth trajectory: The 20% growth this quarter is solid, but can they sustain this as the capital base grows?

Acquisition pipeline quality: The slight decline in acquisition spending isn't necessarily concerning, but I want to see if they're maintaining pricing discipline or struggling to find attractive deals.

The Bottom Line

This quarter perfectly illustrates why CSU remains one of the highest-quality compounding machines in public markets, but also why investors need to think carefully about valuation. The cash generation is exceptional, the business model is intact, and management continues to execute flawlessly.

However, I'd caution against extrapolating historical returns indefinitely. The so-called ‘smart money’ is modeling gradual return compression from the current 20%+ IRRs toward something more sustainable in the 15-20% range over the next decade. Even at those levels, CSU would remain an exceptional business, just not the perpetual 20%+ compounding machine some investors expect.

One thing that gives me more comfort as a CSU shareholder is Mark Leonard and his team’s extraordinary ability to execute almost flawlessly, regardless of market conditions. As a firm believer in their skills as exceptional capital allocators, I’m confident entrusting them with my capital, knowing they’ll continue working to deliver outstanding shareholder returns, even if the pace inevitably moderates over time.

For long-term investors, quarters like this reinforce why CSU deserves a premium valuation. Just make sure that premium is based on realistic expectations about the future, not a mirror of the past.

Thanks for following along.

—Nikotes

The Fair Value Loss due to FX will become Realised Loss if the FX maintained at the same level for the next 4 quarters.

.

Watch out.

.

It is better to adjust Net Income quarterly to monitor.

.

There is another school advocates that Net Incomes are better than Cash Flows when deriving the Long Term Future Cash Flows.

.

FASB was right: Earnings beat cash flows when predicting future cash flows

Ray Ball† Valeri Nikolaev‡

December 2020

https://business.columbia.edu/sites/default/files-efs/imce-uploads/CEASA/Events%20Page/fasb_earnings_beat_cash_flows_when_predicting_future_cash_flows.pdf