Every quarter, the same bear thesis re-emerges for Constellation Software: the company is simply too large to keep deploying capital at its historically demanding hurdle rates. The law of large numbers, they say, will eventually catch up. Every quarter, Constellation responds with its results, and every quarter the thesis gets shelved until the next one. Q1 2026 was no different, in fact, it may have been the most clear rebuttal yet.

Before I get into the numbers, let me briefly set up the optical messiness you’re likely to encounter if you just glanced at the headline figures, because this is a quarter that will genuinely confuse anyone not deeply familiar with CSU’s structure.

The Numbers at Face Value

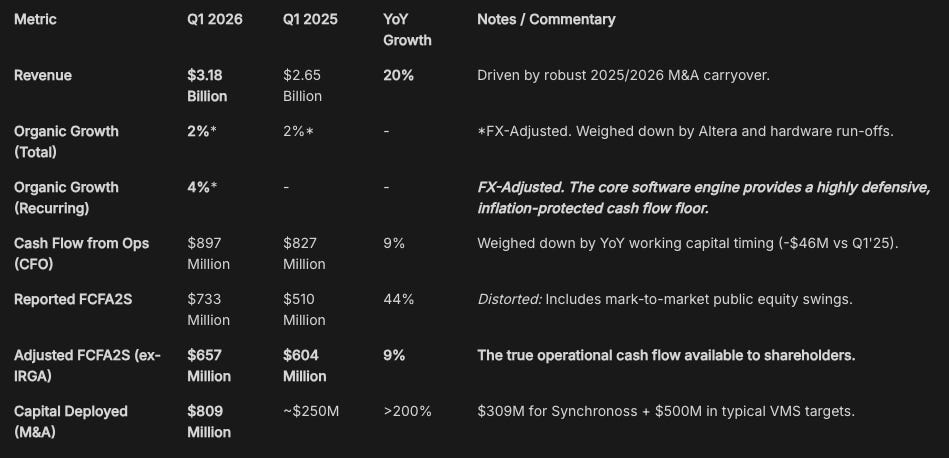

Revenue grew 20% YoY to $3.18 billion. That part is clean. Everything else requires some work.

Headline FCFA2S surged 44% to $733 million, which sounds spectacular, but it’s a distorted number. And headline net income attributable to shareholders came in at $367 million, up 170% YoY, which sounds almost absurdly good, until you understand why.

Both distortions share the same culprit: the IRGA/TSS liability revaluation. I’ll explain this properly in a dedicated section below, because if you don’t understand it you’ll either get too excited or too worried, and neither serves you. The short version is this: strip out the non-cash noise, and FCFA2S grew 9% on an adjusted basis to $657 million. A 9% cash flow growth rate versus 20% revenue growth looks like a wide gap (an it is) but working capital timing and FX explain almost all of it. Adjusted for these, underlying cash conversion is tracking somewhere between 16-18% growth YoY, which is much more consistent with the business’s historical profile.

So the quarter, in terms of cash flows, was not as spectacular as the headline FCFA2S implies, but it was also not as underwhelming as the 9% adjusted figure might suggest at first glance. The underlying business is fine. More than fine, actually.

The IRGA Distortion and the Headline Cash Flow

If you’ve owned Constellation for any length of time, you’re familiar with the complexity that the Topicus spin-out introduced into the financial statements. If you’re newer to the name, this section can help.

When CSU spun out Topicus, it retained a complex agreement, the IRGA, with the Joday Group, the original founders of TSS who hold a roughly 29% minority stake in Topicus. Joday holds a put option to sell their stake back to Constellation. CSU must record this future obligation as a liability, and weirdly enough, the value of that liability is tied to the share prices of Asseco and Sygnity, two public companies in which Topicus holds stakes.

What this means in practice is that CSU’s FCFA2S calculation is now partially held hostage to the mark-to-market movements of two Polish stock exchange listings. This injects equity volatility into what should be an operational cash flow metric.

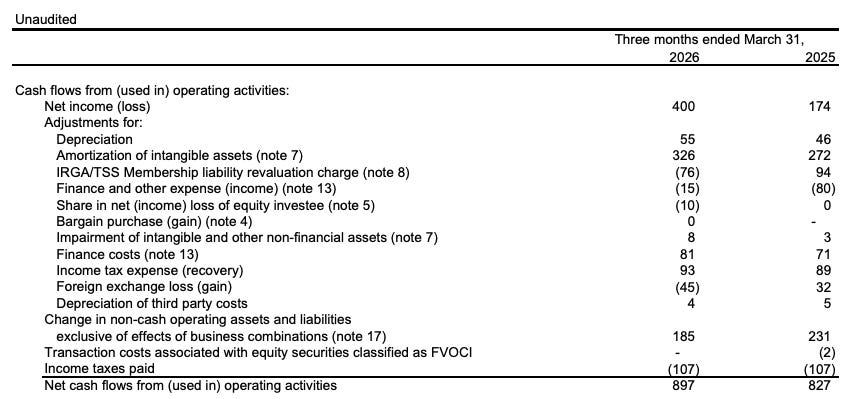

In Q1 2025, Asseco and Sygnity share prices were rising, so the liability CSU owed to Joday increased. CSU deducted $94 million from FCFA2S that quarter to reflect this. In Q1 2026, the same shares declined, so the liability shrank. CSU added $76 million back to FCFA2S.

So, the YoY swing from that one line item alone is $170 million, entirely non-cash, entirely driven by two European share prices that have nothing to do with Constellation’s operating performance.

Strip that out, and FCFA2S grows 9%, not 44%.

I know. Sigh.

Now, the 9% figure itself needs context. Operating Cash Flow (CFO) grew at the same 9% clip, confirming this is the real underlying number. But why is 9% trailing 20% revenue growth so much? The answer is predominantly working capital timing and some FX headwinds. Let’s see :

In Q1 2025, CSU benefited from a $231 million positive swing in non-cash working capital. In Q1 2026, that benefit was $185 million, a $46 million YoY headwind that’s purely a function of the timing of payables, receivables, and deferred revenue. On top of that, FX (Foreign Exchange loss line) went from a $32 million tailwind to a $45 million headwind, a swing of roughly $77 million.

Add back those timing effects, and the underlying cash conversion lands at 16-18% growth YoY, closer to the revenue growth rate than the headline 9% implies. I wouldn’t lose sleep over this quarter’s cash flow print.

Margin Noise, the Classic CSU Playbook and AI

Analysts pushed back on margin dynamics during the call, and CFO Jamal Baksh’s response was, to his credit, completely disarming:

“There were a couple of other acquisitions that were a bit of a drag on margins, like the Q1 cohort of acquisitions themselves were actually a negative margin for the quarter, which, you know, we totally plan to improve them, and it is a typical thing where we improve margins over time.”

This is textbook Constellation. You buy neglected, sub-optimally run assets, you endure a quarter of optical margin drag, and then you apply the playbook to improve them over time. If you’re surprised by this mechanism at this point, you probably haven’t been following the company long enough.

There were two additional minor drags this quarter: hardware margins dipped slightly (43% vs. 46%), and the company utilized more third-party maintenance and coding providers than usual, contributing roughly a 20 basis point headwind. Neither moves the long-term needle.

What I’d actually flag as more interesting is the “forward-deployed engineering” concept that President Mark Miller touched on. Constellation is investing in AI tools not to cut internal costs (probably they are doing that too though), but to expand its presence inside existing customers’ workflows. The initial deployment creates some costs before it creates revenue, which is the right way to think about it.

Mark Miller framed it well:

“I look at these AI tools as an opportunity to do more for customers, not do what we currently do more efficiently, although that will happen in some cases... They’re using them to try to develop more software to actually expand our presence inside of customers, more so than defend our presence.”

I think this is the right posture.

AI at Constellation is a mild margin tailwind over time, not an arms race. R&D expenses are growing more slowly than revenue. There’s no expensive model-training infrastructure race here; it’s productivity tooling applied to the existing developer base in their existing niche verticals.

Also, Miller touched on another interesting point around UI experience stickiness vs AI:

“Customers are obviously hesitant to change their user experience because it’s something that their team uses all day to run their business... Changing how the user interacts with the software is a big decision for a client... We’re generally not taking on very large horizontal companies in many of our niche verticals because that’s sort of how we defend our market position by being small and intimate with dozens or hundreds of customers.”

The businesses CSU owns are intimate, highly specialized deployments with dozens or hundreds of customers. Disruption risk, as Miller noted, tends to concentrate in high-churn, high-attrition markets. That is not CSU’s address.

The M&A Machine: $1.6 Billion in 135 Days

This is the part of the quarter that deserves the most attention.

In Q1 alone, CSU deployed $809 million across acquisitions. $309 million of that was Lumine Group’s take-private of Synchronoss, a classic public-to-private carve-out that required the kind of senior executive talent and multi-geography deal complexity that CSU’s President acknowledged they may not have been able to handle five to ten years ago. The remaining ~$500 million was deployed across dozens of traditional, non-significant private VMS acquisitions spanning aviation, legal, healthcare, and other verticals.

Then, subsequent to the quarter end, CSU revealed in the Subsequent Events note (Page 55 of the filing) open commitments to acquire another $786 million in targets.

Add those together and you have roughly $1.59 billion committed in approximately 135 days.

For context, total capital deployed across all of consolidated Constellation in full-year 2025 (including Topicus and Lumine, but excluding public target acquisitions) was $1.588 billion.

They did in 4.5 months what took them an entire year in 2025.

I’ll be direct: I think this is the most important datapoint in the entire release, because it speaks directly to the bear thesis that Constellation is becoming too large to compound efficiently. The argument goes that as the company generates more and more free cash flow, finding enough quality acquisitions at the IRR hurdles CSU demands becomes structurally harder. Q1 2026 shows that argument is, at a minimum, premature.

The combination of traditional small-VMS roll-ups and large carve-outs via spin-outs (Lumine handling the complex public-to-privates, for example) is working as a complementary system. And now there is a new lever in play.

PEMS: The Strategy That Could Structurally Widen the TAM

Management formally began accounting for the Permanent Engaged Minority Shareholder (PEMS) strategy this quarter, reflected in a $32 million cash outflow under “Purchases of investments and other assets”, which appears to represent the accumulation of a public stake in Sabre (maybe something else?).

The concept is worth understanding carefully, because it changes the TAM for capital deployment in a meaningful way. Under the traditional CSU model, the company acquires 100% of a private vertical software business. PEMS is different: CSU takes a minority public stake with an active governance role, the same way Topicus holds minority stakes in Asseco and Sygnity.

The hurdle rate is the same. The CFO was explicit about it:

“In terms of PEM, the hurdle rate is the same. However, the modeling in terms of the weighting of worst-case versus winner-case are gonna be probably much more dispersed, and so will probably result in a lower price, but the hurdle rate is the same.”

The key implication of the PEMS strategy expanding is that it opens up public market targets at scale (businesses that CSU could never have acquired outright due to size or public market premiums) as a new avenue for disciplined capital deployment. And because CSU lacks full control, they discount the modeling appropriately, which is intellectually consistent.

There is also a reporting wrinkle here that investors should understand. Current FCFA2S does not capture CSU’s pro-rata share of cash flows from PEMS investments. Management is actively discussing the introduction of a new internal metric, likely “Economic Net Income” to give investors proper credit for these cash flows. CSU’s CFO said as much:

“For these types of PEM investments, we would actually look at our pro rata share of their ultimate cash flows, which doesn’t show up in our current statements. It’s something we’re thinking through right now to try to maybe give you investors the same metric that we’re using internally.”

The implication is straightforward: current FCFA2S understates Constellation’s true earnings power to the extent PEMS investments are accumulating and generating cash. How much understated is hard to say right now given the early stage of the strategy, but it’s a direction of travel worth tracking.

Deconstructing the Ecosystem: CSI Core vs. Spin-Outs

Because Constellation is increasingly a holding company, it’s worth running the lens across its three constituent parts separately.

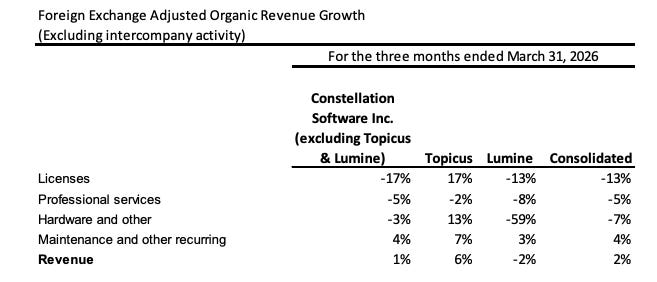

CSI Core (ex-Topicus/Lumine) generated $2.46 billion in revenue, with total organic growth at 1% but recurring maintenance organic growth at +4%. The Core deployed $478 million into traditional private VMS acquisitions and generated $548 million in operating cash flow. This is the mothership.

Topicus generated $507 million in revenue with +7% recurring organic growth and +23% total revenue YoY, the highest organic growth engine of the three, continuing to demonstrate the opportunity in European vertical software and beyond. Topicus is executing well from a lower market cap base. A mini-CSU on its prime.

Lumine generated $208 million in revenue, growing +3% recurring organic gorwth despite selling to a declining industry and executed the Synchronoss take-private to the T, showing its ability to absorb a large, complex transaction cleanly. Once again, capital allocation at its finest led by their excellent CEO and founder D. Nylan.

The fact that all three segments are operating simultaneously (each with its own M&A pipelines, talent, and organic growth profiles) is what makes Constellation difficult to replicate.

The other piece worth isolating is Altera, the healthcare asset carved out from Allscripts in 2022. Altera generated $147 million in revenue but printed -13% FX-adjusted organic growth. Management has never pretended otherwise: Altera was acquired for its cash flow and value, not its growth profile, and the deliberate rundown of unprofitable customer relationships was part of the thesis from day one. Excluding Altera, consolidated organic growth would look visibly better. I’d keep an eye on when this rundown bottoms out, because at some point Altera needs to stabilize and start contributing rather than dragging.

The Risks

The first is PEMS execution risk. Being an activist minority shareholder in a public company is a fundamentally different operational challenge than owning 100% of a private $5 million ARR business. If management teams at PEMS targets resist CSU’s governance influence, capital could be trapped in underperforming positions with limited exit flexibility. It’s early days, and I’d watch how the Sabre stake evolves before drawing conclusions about the strategy’s durability.

The second is leverage at the spin-out level. Debt without recourse to CSI stands at $2.51 billion. As Lumine and Topicus take on standalone debt to fund larger transactions, rising interest rates at the subsidiary level could pressure the cash flows ultimately distributed up to the parent. Not really a concern given the capital allocation excellence of the spin-outs and CSI, but worth monitoring as deal sizes grow.

The third is Altera stabilization. At -13% FX-adjusted organic growth, the question is how long the customer rundown continues before the asset reaches a normalized base. The thesis was always cash flow, not growth. But the drag it creates on consolidated organic metrics has a limit to how long it remains an acceptable explanation.

What This Quarter Tells US

To summarize where things stand after Q1 2026, here are the key theses this print confirmed or refuted:

The “too big to grow” thesis took another beating. $1.59 billion in capital deployment in ~135 days, at the same IRR hurdles, across dozens of verticals and deal types. The machine is not slowing down.

The recurring revenue core is healthy. 6% (4% FX-adjusted) organic growth in maintenance is consistent with the company’s track record of CPI-linked pricing and near-zero churn in mission-critical software.

The FCFA2S distortion and accounting complexity is real. Once you understand the IRGA mechanics and strip out working capital timing and FX swings, underlying cash conversion is tracking at 16-18%, not the headline 9% and not the distorted 44%. Accounting noise is real, but management is trying to do his best to clarify it with upcoming new KPIs and unaudited reports full of details.

AI is not a threat to Constellation’s model; it’s (potentially) a mild tailwind. UI stickiness in mission-critical workflows, ultra-niche deployments with high switching costs, and management’s pragmatic view of AI as a tool to “do more for customers” all point in the same direction.

PEMS is early but structurally important. If it scales, it meaningfully widens the TAM for capital deployment in a way that the traditional private VMS model alone could not.

The accounting complexity is real and will only grow as Constellation’s structure becomes more intricate. That complexity is going to continue to create noise with messy quarters, distorted headlines, and confused observers. For long-term investors willing to do the work to look past it, that complexity is arguably part of the opportunity. The underlying business is as clean as ever.

Thanks for following along,

—Nikotes

Unlock Premium Content – For just $0.39/day ($12/month) or $0.27/day ($100/year)!

🔗 Portfolio Corner - 🗓️ Monthly Updates (Last Update: 3-May-2026)

Great article! Thanks again.

Wonderful piece, Nikotes. Thanks for sharing.