"If we look at the market demand... this has motivated our customers to increase their CapEx but also accelerate all their plans. This really creates a need for more systems basically starting this year... our customers are getting long-term agreements with their own customers... Because they have what I would call a quite unprecedented visibility on what will happen to the market." — Christophe Fouquet, CEO

Yes, don’t blink twice, you read that correctly.

AI is creating unprecedented demand visibility for what is arguably the monopoly business with the greatest long-term visibility into customer roadmaps anywhere in the semiconductor industry.

You could argue that, as an investor, this quote alone tells you everything you need to know from ASML’s Q2. Close the earnings deck, hold the stock, and check back in 2027 to see how the backlog evolves beyond 2028.

But I think it’s worth digging a little deeper into the why, the how, and the what behind that statement.

Financial Results

Note: Charts below as shared from 🔗 SemiAnalysis Source

The Installed Base Management Surprise

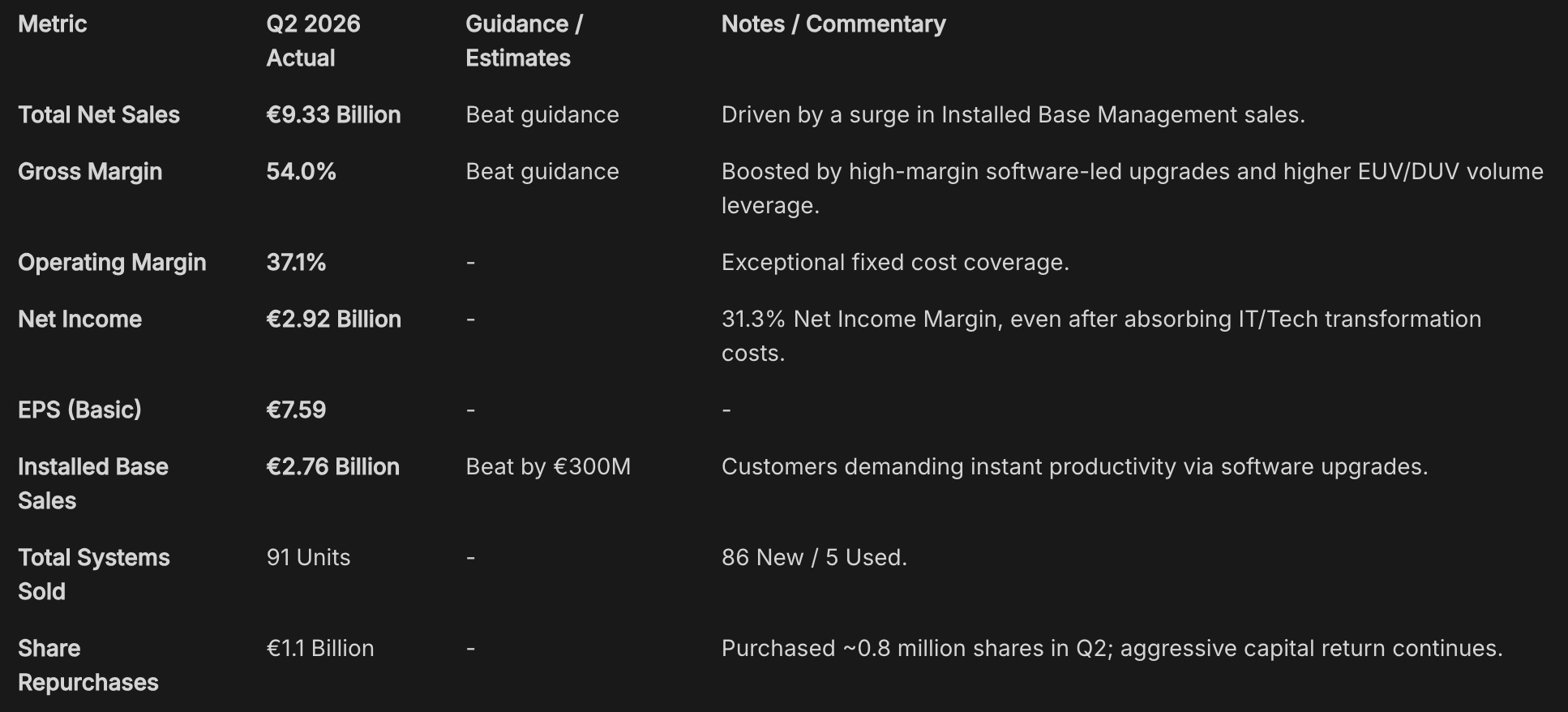

Most of the post-earnings attention has focused on the guidance raise, and rightfully so. But the €300 million Install Base Management (IBM) or Net Service and Field option sales upside is arguably the more interesting story.

The main driver of the gross margin beat this quarter was, once again, the installed base management (IBM) business, which came in at €2.8 billion, roughly €300 million above what management had guided. CFO Roger Dassen explained it during the CC:

"Main reason why it was above guidance is the Installed Base business. The Installed Base business came in at €2.8 billion. That is €300 million more than we expected. As a result of the fact that customers are really looking for productivity enhancements and therefore the upgrade business was quite high... We're increasingly in a position to give that to customers because a lot of the upgrade business is software led. So it doesn't take a lot of machine time." — Roger Dassen CFO

For those less familiar, IBM refers to the software-led upgrades and services ASML provides on its already-installed fleet of machines, not new system shipments. When customers can’t get new tools fast enough (and right now, they can’t), they turn to ASML to extract more throughput from what they already have.

The NXE:3600 to NXE:3800 upgrade cycle that I’ve been discussing for some time in past earnings digests is clearly accelerating. These upgrades carry higher gross margins than system sales, which is precisely why IBM over-delivery this quarter drove a corporate margin beat despite no major surprise on the system revenue line.

I think this is a business that continues to be underappreciated. A software-led upgrade flowing through the IBM line carries better margins than a new EUV system, and as the installed base grows (which it will, given the shipment ramp in H2), the IBM business will only get larger in absolute terms. I don't think the market has fully internalized this as a structural rather than cyclical driver of margin expansion.

Also, what this quarter told us is that demand is pressing up against physical constraints and customers know it (nod to TSMC 😉). When you’re scrambling to convert existing tools rather than waiting for new ones, it tells you something about the urgency of the capacity build happening right now. It does confirm the tightness of the supply/demand dynamic in a way that quarterly system sales numbers simply can’t.

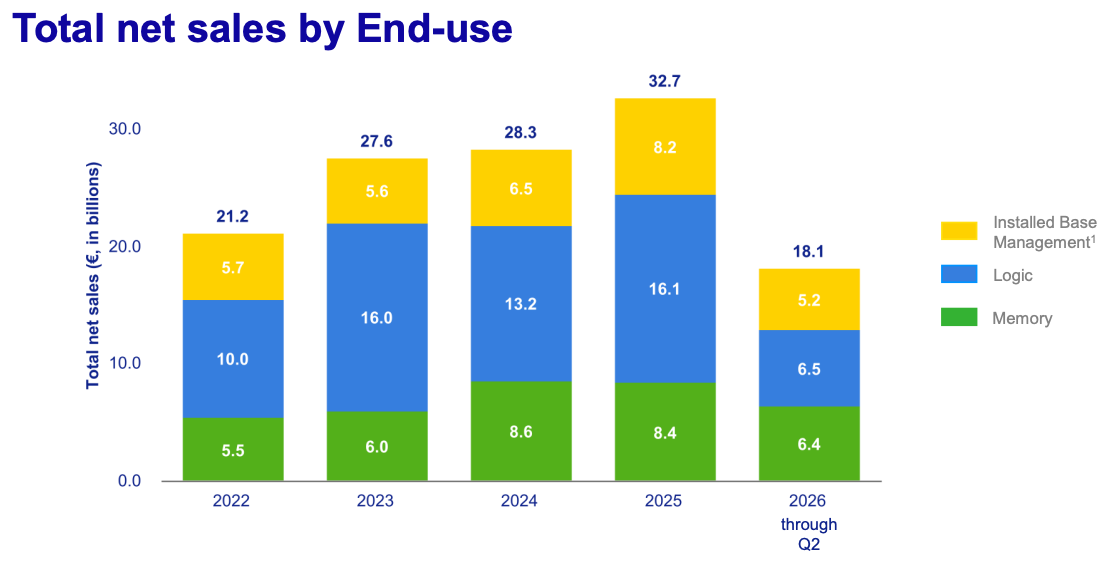

Logic & Memory: Different Stories, Both Pointing the Same Direction

Management provided some specific color on end markets that’s worth sitting with.

On the Logic side, management is expecting roughly 25% growth in 2026, driven almost entirely by advanced node capacity additions at the sub-5nm level. What struck me was Christophe Fouquet’s comment that the 2nm ramp is being pushed “as aggressively as possible” by foundries, and that customers are already planning capacity for 1.4nm.

This is not incremental. Each successive node requires more EUV layers, more critical exposures per wafer, in other words, more litho intensity. The thing is that the AI accelerator buildout has effectively compressed the node transition timelines that used to stretch across many years. That compression is a structural tailwind for ASML’s unit economics that I don’t think is fully reflected in how people are modeling the 2030 guidance.

Memory is the more surprising story.

If you had told me at the start of 2026 that memory would be ASML’s fastest-growing segment, I’m not sure I would have put it at the top of my list of likely outcomes. But that’s exactly what’s happening. Management expects memory revenue to grow approximately 75% YoY in 2026, outpacing logic growth of ~25%. Fouquet explained the dynamic:

“If we look at the price of Memory today, either for DDR or for HBM, there is a clear need for more supply. This is translating into, again, acceleration of capacity plans from our customers... the latest nodes are calling for more litho, for higher litho intensity, both on EUV but also advanced immersion.” — Christophe Fouquet, CEO

The key phrase here is "higher litho intensity." As memory manufacturers move to the latest nodes (particularly in the context of HBM demand driven by AI training), the number of lithography layers per chip is increasing. This is structurally positive for ASML across both EUV and advanced DUV immersion tools, and it's a dynamic I expect to continue as the AI infrastructure buildout compounds over the next several years. The fact that DRAM customers are adopting EUV at scale is a validation of something I've been watching for some time: litho intensity doesn't go backward. It goes up.

I’ll note that memory has historically been the most cyclical part of ASML’s business, but what we’re seeing with HBM is a structural increase in litho intensity that looks more durable than a typical upcycle. I remain cautious about extrapolating memory numbers, but the litho intensity shift appears sustainable.

“Unprecedented Visibility”

I want to dwell on this phrase because it’s being thrown around in market commentary without much scrutiny.

The gist of it (and I’m paraphrasing rather than directly quoting the release) is that major foundries are locking in long-term capacity agreements with hyperscalers and AI chip designers, and those agreements are flowing back through to ASML as extended-horizon orders.

Management noted they are already “close to receiving all the EUV orders” they need for 2027, and are actively investigating a second 30% capacity expansion for 2028 on top of the 30% expansion already announced for both Low-NA EUV and DUV immersion for 2027.

“If we look into more detail starting with 2027, there we are pretty much already close to receive all the EUV orders we need for 2027. This is with us adding about 30% capacity for EUV in 2027 versus 2026. When we look at 2028, we have received already a large number of orders from our customers for EUV. This has also invited us very strongly to investigate another 30% increase in our EUV capacity for 2028.” — Fouquet CEO

I would note that this is the same management team that, just a few quarters ago, was unable to confirm 2026 growth due to geopolitical uncertainty.

The shift in tone is very telling and I think it’s worth contextualising what a 30% capacity increase actually means for a company like ASML. The supply chain here, i.e. Carl Zeiss for optics, Trumpf for laser sources, VDL for mechatronics, etc. is highly specialized and not easily scaled on short notice. The fact that management is announcing this now tells us something about the visibility they have into demand.

I think the catch/risk is execution. If there’s a bottleneck anywhere in that chain, you don’t get the revenue and management knows this better than anyone. I would treat this as the primary operational risk in the medium term.

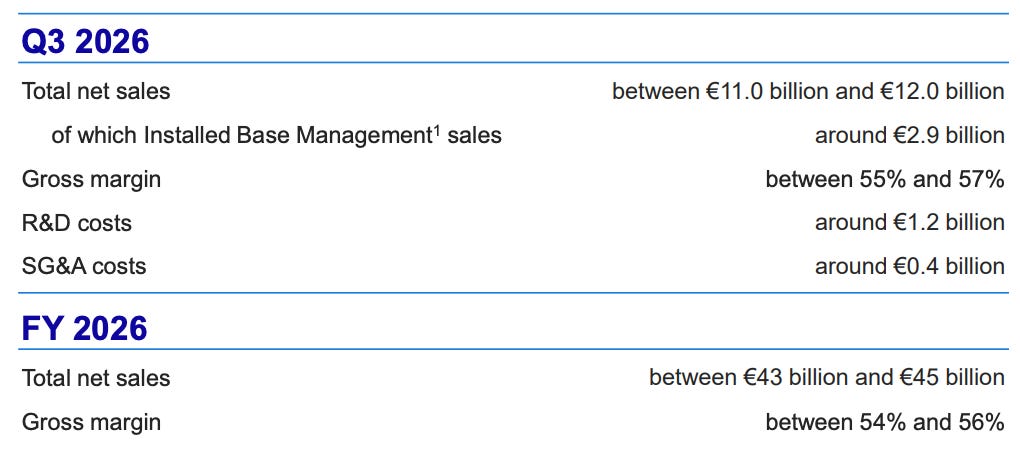

On the 2026 Guidance Raise and What It Means

€43–45 billion in revenue for 2026 implies a steep H2 ramp. H1 sales is at €11.8 billion and Q3 guidance alone is €11–12 billion. That’s a number that would have seemed extraordinary not long ago. Some investors will fixate on execution risk and they’re not wrong to flag it. But I’d rather focus on what the guidance raise tells us structurally.

So, let’s do the EUV Math to know what H2 needs to look like.

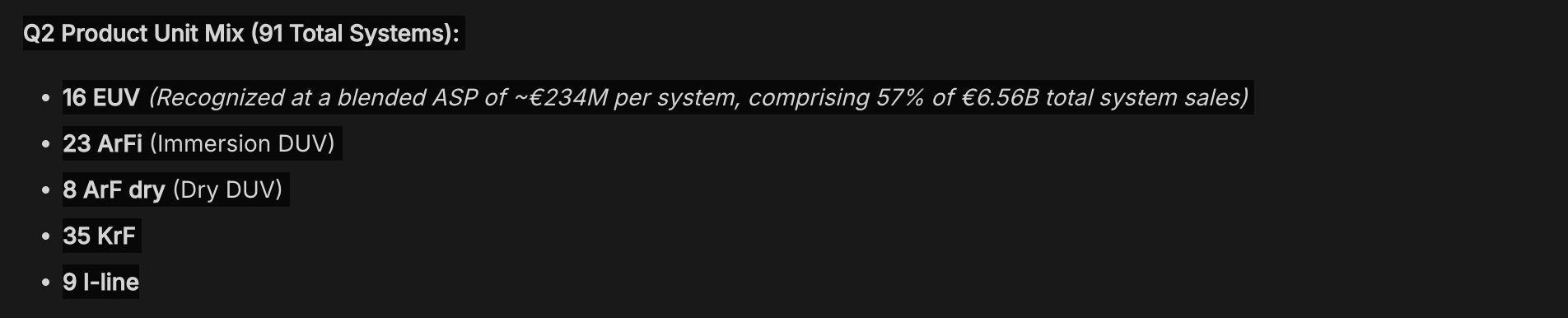

Management expects roughly 65 Low-NA EUV systems for the full year. H1 saw 29 Low-NA systems shipped, which means roughly 36 are expected in H2, a 24% acceleration half-over-half. Total EUV revenue is guided to grow ~45% for the full year, which, applied to the €11.6 billion 2025 base, implies approximately €16.8 billion in EUV revenue for 2026. Note that this excludes any additional High-NA systems as the company did not provide a full-year High-NA shipment target.

On the other hand, ASML’s 2030 guidance, set at the last Capital Markets Day, framed a range of €44–60 billion in annual revenue by the end of the decade. The midpoint of the new 2026 guidance sits squarely inside that range, four years early!

Management has now announced a new Capital Markets Day for June 2027 specifically to “revisit assumptions” in light of the AI demand acceleration. I think most people know what that means: the long-term models are moving up. Whether they move up by 10% or 30% is a question worth thinking about, and I intend to write more about this after the event.

“High-NA is Too Expensive” + “ASML has No Pricing Power”: Two Bear Theses Put to Rest ?

I’ve been somewhat cautious about High-NA EUV adoption timelines because the technology is still young and I don’t think it’s prudent to model aggressive adoption without proof of commercial maturity. During ASML’s Q2, we got a meaningful data point. Intel Foundry has officially qualified High-NA EUV for select layers on its 18A process, meaning the tool is being used in production today.

“Intel is basically now using High NA in production on their most advanced products. So it means that some of the products you buy today from Intel have been created with an High NA machine. So this is, of course, a very important milestone. This is the proof of the maturity of the tool.” — Fouquet CEO

This matters because one of the recurring bear arguments has been that High-NA (a machine that costs upwards of $350 million per unit) is too complex and too expensive to achieve broad adoption in the near term. Intel’s qualification doesn’t fully invalidate that concern (broad adoption will take years), but it does demonstrate that the tool is capable of HVM. And once the economic case firms up through productivity improvements and rising wafer demand, I would expect TSMC and Samsung to follow. Fouquet mentioned they expect to “enter that discussion with all customers” soon.

The long-term productivity argument I’ve been making on High-NA remains intact: as throughput improves (and it already has, significantly, from the initial NXE:5200 specifications), the cost/wafer equation shifts further in High-NA’s favor. Taking today’s specifications and extrapolating them to 2028 or 2030 adoption rates is, I’d argue, not the best way to model this.

One more point worth highlighting.

Shortly after ASML’s Q2 2026 results, reports started to circulate that the company is planning to raise prices on its lithography equipment. According to those reports, ASML has discussed higher EUV pricing with TSMC and informed some customers, including Chinese chipmakers, that DUV system prices could increase by around 10%.

If accurate, this puts another common bear argument to rest: that ASML’s tools are already “too expensive.”

In reality, the opposite has arguably been true for years.

Relative to the enormous value its machines create: higher yields, lower cost per transistor, and the ability to manufacture leading-edge chips. ASML has historically been one of the most economically generous suppliers across the wafer fabrication equipment ecosystem. Its pricing has never fully reflected the mission-critical nature of its technology or the extraordinary value it delivers to customers.

China: The Overhang That Won’t Disappear

Management maintained their guidance that China will represent approximately 20% of total 2026 sales. The complication is that because the overall revenue pie is now much larger than expected, the absolute dollar amount flowing to China has increased from estimates of roughly €7–8 billion to approximately €8.6–9.0 billion. Management characterized this as primarily domestic-led logic demand, which is somewhat reassuring, but the geopolitical risk vector here remains.

My view on this hasn’t changed: geopolitics for ASML is a two-sided coin. Restrictions hurt in the near term, but the broader push for domestic semiconductor manufacturing across the US, Europe, Japan, and eventually elsewhere is a long-term tailwind for the company. The question is always timing and severity of the short-term pain versus the long-term benefit. I don’t think China becoming 20% of sales is alarming on its own, but I do think it’s worth monitoring closely.

What This Quarter Put to Rest

To close, I think the most useful thing I can do is list the bear theses that this quarter weakened:

“ASML doesn’t benefit from AI the way Nvidia or TSMC does.” The 75% memory growth, the accelerating Logic node transitions, and the unprecedented order visibility into 2028 are direct expressions of AI-driven capital expenditure. The relationship is indirect but increasingly measurable.

“High-NA is too expensive and not ready for production.” Intel’s 18A qualification is a real data point. The debate about Low-NA multipatterning vs. High-NA single patterning is not closed short-term, but the commercial viability of High-NA is no longer (I’d argue it’s never being) theoretical longer term.

“Memory EUV adoption is a cycle, not a structural story.” HBM litho intensity is different from prior DRAM cycles. The data management provided is consistent with what industry experts have been arguing: rising layer counts per node are a durable tailwind, not a one-time uplift.

“The 2030 guidance is too wide and uncertain.” If we’re already tracking toward the low end of the 2030 range in 2026, the guidance revision scheduled for mid-2027 will be interesting. I’m not ready to model specific upside figures yet, but the structural direction is clear.

What this quarter didn’t resolve is timing.

A business with lead times exceeding a year, products priced in the hundreds of millions, and a supply chain with clear constraints is always going to have quarters where recognition shifts around. That, in my opinion, won’t change, and I’d encourage investors to remain focused on the multi-year trajectory rather than the specific cadence of any given quarter.

The ASML story here has always been measured in years, not calendar quarters. And I suspect it will be kept this way for the foreseeable future.

Thanks for following along,

—Nikotes

Unlock Premium Content – For just $0.39/day ($12/month) or $0.27/day ($100/year)!

🔗 Portfolio Corner - 🗓️ Monthly Updates (Last Update: 25-Jun-2026)